The Coordination Paradigm

You know the saying: “Don’t fight the Fed”. It basically means that when the Fed isn’t your friend – hiking rates or otherwise tightening – you shouldn’t be too optimistic. Of course, it also works the other way. When the Fed is your friend – cutting rates or otherwise loosening – then you shouldn’t be too pessimistic.

It is powerful. This is why so much care is given to monetary policy.

One of the features of the 2022 bear market was that there was no safe haven:

- Stocks were in a bear market (obviously)

- Bonds followed

- Alternatives eventually saw markdowns

- There a real estate scare (BREIT)

- A bank blew up (SVB)

- Neither hard nor digital gold kept their value.

Part of the asymmetry was due to coordination of central banks across the globe. Every geography – in the name of fighting inflation – had a hostile central bank. There was nowhere for money to hide.

This asymmetry, albeit to a lesser degree, continued after inflation peaked. There was a period during mid-2023 and early-mid 2024 where most banks were on hold. Then a period where all banks cut rates back to neutral

The Dispersion Paradigm

So far in 2026, we’ve had four central banks hike: European Central Bank (ECB), Bank of Japan (BoJ), Bank of Norway (BoN), and Reserve Bank of Australia (RBA).

Again… I don’t think that was a wise move… but what do I – and the rest of financial history – know about hiking into an energy shock? Nothing… except it has never once resulted in the desired outcome without serious economic hardship.

As for the U.S., the Federal Reserve is on hold with a bias toward hiking (I don’t see it this year, but that is the consensus). The People’s Bank of China (PBOC) is moving toward easing.

The old era of asymmetry and coordination is over.

Dispersion of Outcomes

It is easy to make broad calls on stocks when all the central banks are doing the same thing:

- All easing → bullish

- All tightening → bearish

- Some tightening; some easing; some holding → [?]

That last bullet is where we are today. In my opinion, the higher dispersion in monetary policy begets a higher dispersion of outcomes. In plain english, I anticipate we’ll see a lot more “big winners” and “big losers”.

It has never been more important to do your homework to avoid the latter.

Homefield Bias

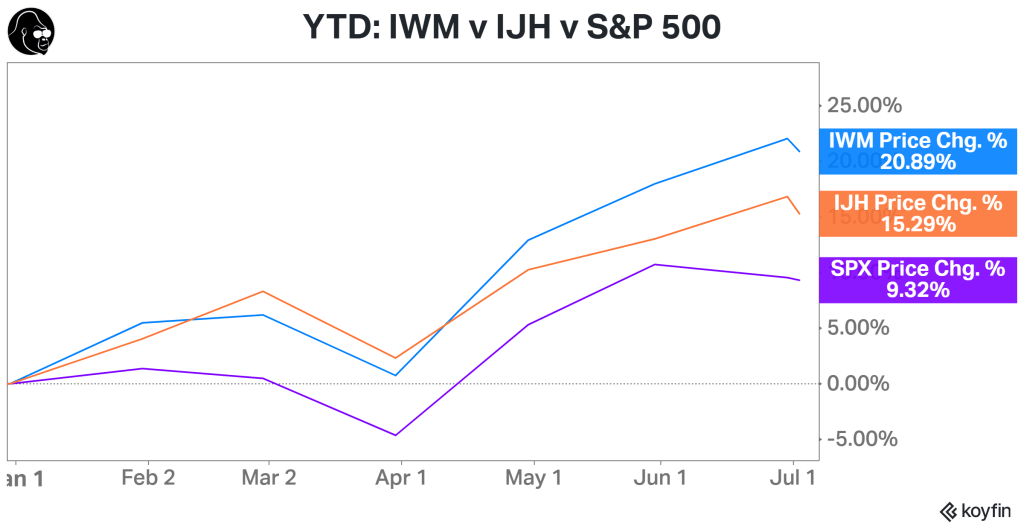

Personally, I believe U.S. markets remain the place to be. We’re really seeing it in the Russell 2000 (IWM) and U.S. Mid Caps (IJH).

Did you know that small and mid caps (“SMID”) is outperforming large cap… by like a lot?

😤 Neither did I 😤

IWM/IJH names are more leveraged to U.S. growth, whereas the S&P 500 has a multinational tilt. The outperformance tells the story: domestic U.S. is hot.

Furthermore, when you take a look at some geographies abroad, like India (INDA), where the potential for an oil-related fallout is relatively elevated, the stage is set for domestic U.S. names to replicate their outperformance in the second half.

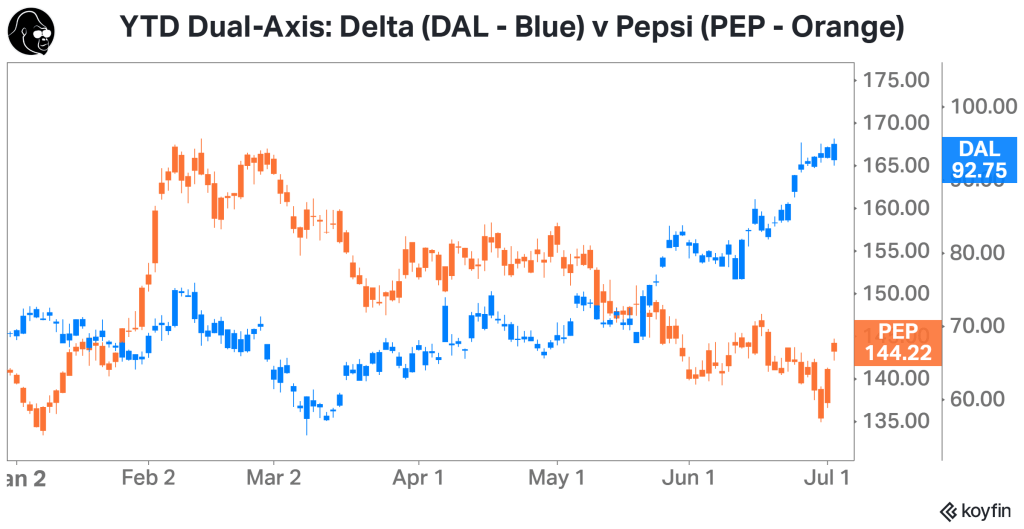

A Tail of Two Stock: Risk-On

Pepsi and Delta report earnings this week, and they couldn’t look more different. Delta is at a 52W high and Pepsi at a 52W low.

The former makes a majority of its money on expensive first-class seats; the latter on sugar-water and savory snacks priced for the masses. The former thrives when economic concerns are low; the latter when economic concerns are high. The message is clear:

There is no interest in the safety offered by traditional staples. We’d rather position for additional upside levered to a strong economy.

This is not risk-off behavior. This isn’t fear. However, it isn’t greed either. In my opinion, right now, risk appetite is healthy without being frothy. For example, while many ARKK names are set up well technically, there haven’t been many blow-off tops in low-quality names.

Concisely, we’re in a good place to start the second half of 2026. I hear negativity from certain corners about the economy. For now, you can safely ignore them.

Key

Macro Economic Events

Corporate Earnings

High Importance

See Note Section Below For Additional Insight

Monday

US Services PMI (June) | No Est. Available; Prior 50.7 | 09:45

Tuesday

None Scheduled

Wednesday

Federal Open Market Committee Meeting Minutes | 14:00

Thursday

PepsiCo (PEP) | BTO

Weekly Jobless Claims (Week of July 4) | Est. 218K; Prior 215K | 08:30

Friday

Delta Air Lines (DAL) | BTO