The Real Test Begins

While we had the soft launch to the second half of 2026 last week, the full launch starts now. The money centers and investment banks get us going in earnest when they report Tuesday, and momentum is strong in the sector.

Two ways to view it; neither are incorrect:

- Price implies expectations are high; post-earnings downside is a real risk.

- Price implies there is more good news to come; post-earnings upside is a real risk.

Regardless of your interpretation, this is true: momentum is a strong market factor. You get a dip that doesn’t materially alter the momentum, dips can be bought. We’ve seen it through the year all across semiconductors.

Let’s not forget, financials were a consensus long coming into 2026. Positioning got wiped out as the sector experienced a 15% decline in Q1. The bullish thesis abandoned due to the U.S.-Iran war flattening the yield curve (how loan books make money) and raising the risk of delaying high-profile IPOs (no one wants to IPO during periods of uncertainty; IB fees). Clearly, positions are being rebuilt; earnings could be the catalyst for the payoff. Here’s why I am optimistic.

IPOs and Debt Issuance

Fees from investment banking (IPOs) and corporate banking (bonds) are going to be a huge.

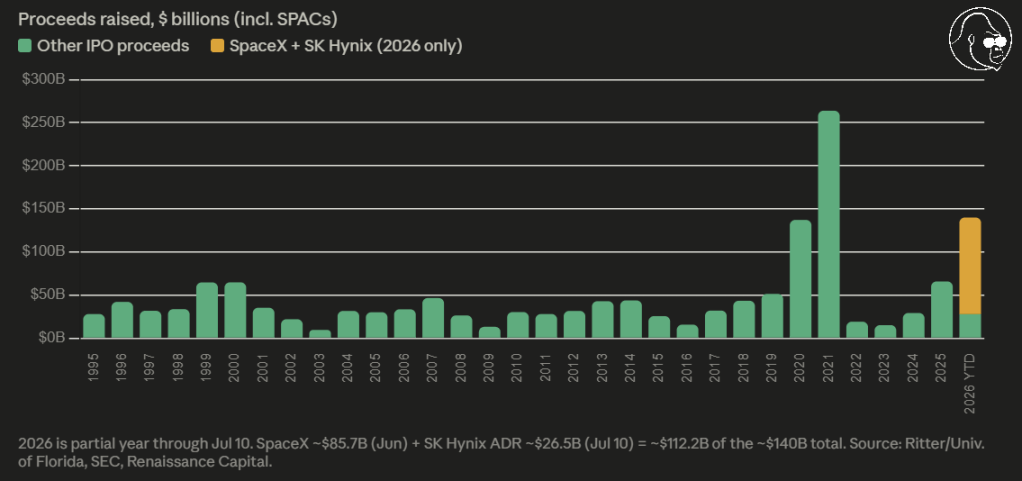

If 2026 were to end today, it go down as a historic year for IPO-dollars thanks to Space X and SK Hynix (ADR). If that weren’t enough, Nvidia, Alphabet, Amazon, Meta, and Space X all tapped the debt market; another fee-based revenue stream that moves the needle for the financials.

Plenty of time for the remaining hyperscalers to give into peer-pressure and do the same. Furthermore, Anthropic and OpenAI remain in the IPO pipeline; guidance secured.

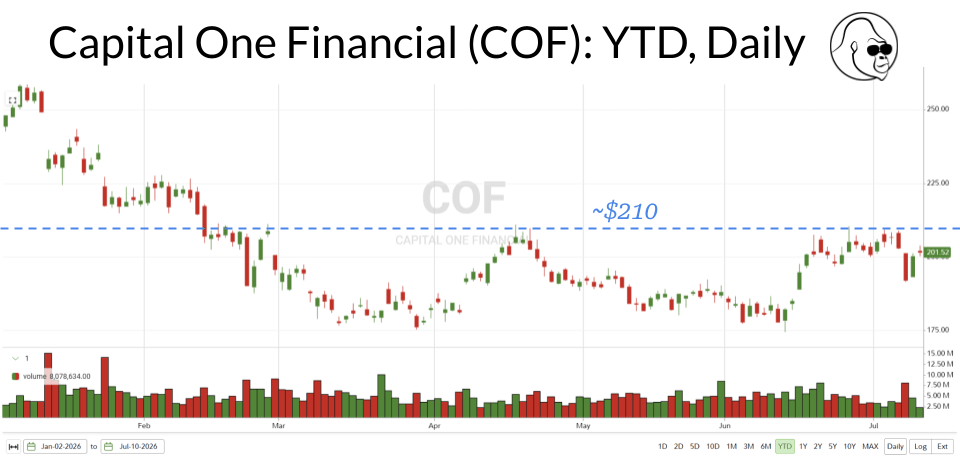

No Consumer Trapdoor

As for credit risk and spending associated with “the consumer”, Capital One Financial (COF) – the bellwether for subprime credit in the U.S. – is well-off of the lows and appears to be positioning for a breakout back to (higher) pre-war prices. As such, I expect the story of “resilience” to remain in tact, removing a potential downside catalyst.

Yield Curve Bottoming

And finally: if the yield curve (10Y-2Y) has bottomed for the year, watch out. That’s what killed the trade in the first place — oil-driven inflation had the 2YR and Fed Funds futures pricing hikes while the 10Y couldn’t keep up. That catalyst hasn’t fully played out yet. Earnings can’t move the yield curve, but it’s the one external input you need to watch if you’re long the banks.

In my opinion, the fundamentals marry up with the technicals. All that’s left is the honeymoon.

Ready To Get Hurt Again

I am stupid long the financials — not just tactically, strategically. It’s part of my overall allocation. I want this to work, and I have reason to think it will: the fundamentals (earnings, forward earnings) and the technicals (the chart) are aligned. That’s a high-probability setup. Even so… sometimes it still doesn’t work: earnings don’t fully validate the setup, an orange swan event, etc.

It’s happened to me before; I imagine it will in the future. I am bullish nonetheless and ready to get hurt again.

Key

Macro Economic Events

Corporate Earnings

High Importance

Monday, July 13

None Scheduled

Tuesday, July 14

Bank of America (BAC) | BTO

Citigroup (C) | BTO

Goldman Sachs (GS) | BTO

JPMorgan Chase (JPM) | BTO

Wells Fargo (WFC) | BTO

June Consumer Price Index (CPI) | 08:30

Federal Reserve Board Chair Kevin Warsh Presents Monetary Policy Report to U.S. House Financial Services Committee | 10:00

Wednesday, July 16

ASML Holding (ASML) | BTO

Progressive (PGR) | BTO

June Producer Price Index (PPI) | 08:30

Federal Reserve Beige Book | 14:00

Thursday, July 17

Prologis (PLD) | BTO

TSMC (TSM) | BTO

UnitedHealth Group (UNH) | BTO

Retail Sales (June) | 08:30

Weekly Jobless Claims (Week Ending July 11) | 08:30

Netflix (NFLX) | ATC

Friday, July 17

None Scheduled