Micron Killed the Magnificent Seven

The Magnificent 7 (M7) isn’t the AI trade anymore.

That mantle belongs to semiconductors, semi equipment, and data-center industrials (energy, infrastructure, etc.).

The market has moved on.

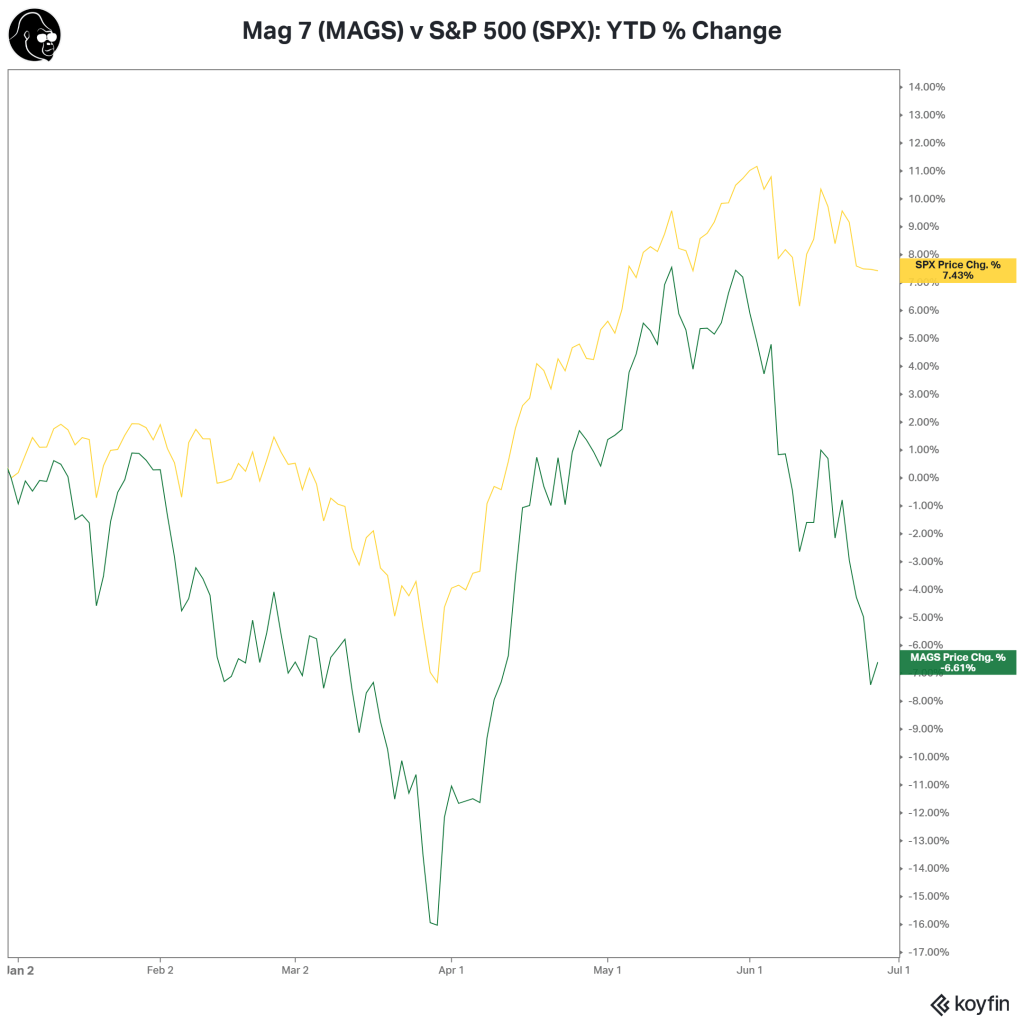

For everyone who warned that Mag 7 concentration would sink the market, keep holding that L. The Mag 7 are now the Lag 7: down YTD, while the S&P 500 sits within 5% of its ATH.

Micron did this. The mechanism: SCAs, Strategic Customer Agreements.

The name undersells it… SCAs have materially changed the AI trade and dealt a serious blow to what were the most invincible stocks in the market. Here’s Micron CBO Sumit Sadana explaining them on the earnings call:

There are annual volume commitments for each of those years. And the take-or-pay means that whether they want to purchase the bits or not, they are obligated to pay for the price times the volume. The price itself for a lot of these large agreements has a price band. There is a price ceiling and a price floor. The price gets negotiated every quarter based on market conditions, the price cannot exceed the ceiling no matter what, cannot go below the floor no matter what.

Translation: customers are locked into multi-year, binding, non-cancelable volume commitments. The old fear – double/triple ordering, then walking away when demand caught up – is off the table.

16 customers have signed on. By 2029, SCAs will represent 40% of MU’s revenue. Memory’s cyclicality needs a rethink: these agreements give visibility into future earnings the industry has never had before.

That doesn’t make memory acyclical, but the leverage required to pull this off sends three messages:

- We aren’t close to the top in memory prices.

- Memory customers don’t expect new supply soon.

- Capex for companies with memory (HBM/DRAM) as an input isn’t going down.

Number three is the Mag 7’s problem. If the memory pricing cycle isn’t close to a peak, margins for memory-buyers are in serious jeopardy. Apple just announced it would raise prices to help offset memory price increases. If AAPL — one of the largest buyers of memory — can’t secure a price, no one is safe.

That puts margins front and center this earnings season. Will the pressure show? If so, how much more pain is coming. If not, will the market believe it?

A Last Breath or A Breather

My opinion, a breather.

SCAs warrant a rethink of the length of this memory cycle, but it does not mean the end of a cycle. Put another way, the risk to margins – which exists so long as memory producers can exert extraordinary pricing power – will not continue in perpetuity but will clearly be a factor longer than previously anticipated.

Here are a few ideas I’ve heard on how this resolves itself… and my rebuttals:

- New Supply From A New Fab → Too long. That takes years, billions of dollars, and a lot of human capital. If new supply has to be the hero, we’ll be waiting a while.

- Hyperscalers Find Ways To Use Less Memory (Efficiency) → Seen it. TurboQuant, Google’s extreme memory compression method for AI models, was supposed to suppress demand. It increased it instead; Jevons Paradox in action.

- The M7 says, “enough is enough” (Demand Destruction) → Possible, but unlikely in the near-term development given the SCAs.

Over the past half decade, bears have called for the end of tech hegemony numerous times. It has yet to come to fruition.

In my opinion, this threat to hyperscalers’ margins doesn’t seem sustainable; however, I am not sure what changes the the market’s mind. But, I do know the market moves a lot faster than it used to. News travels faster; money moves with less friction; markets are more nimble. Whatever changes is more likely to be abstract than concrete, and it will before anyone is sure why it is happening. Put another way: blink at the wrong time, you’ll miss the recovery.

Don’t Blink

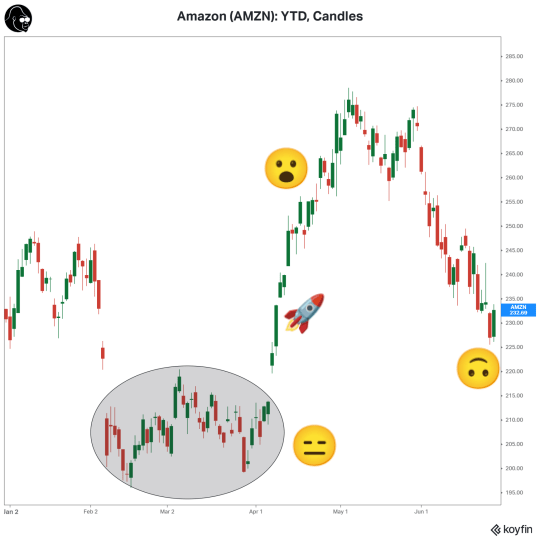

It happened with Amazon. I am still not exactly certain what caused the rapid island reversal a few months back. But, if you blinked, you missed it.

That’s why I am staying with Apple, Alphabet, and Amazon. But, until we see a sentiment shift…

Bear Market Rules Apply

Even counting Friday’s rally, every Mag 7 name is in a correction or worse (>-10%). The charts look terrible. First glance, this is a bear market rally/bull trap/countertrend move; whatever vernacular you prefer to define a rally that fades. Market logic right now: reward check-cashers, punish check-writers. The hyperscalers are check-writers, and they’re exhibiting bear market behavior even if they are not in a 20% drawdown. Here are the rules:

- Good news doesn’t matter — news is only getting worse.

- Upside moves are quick and explosive, then quickly fade.

- Downside moves are slow, divisive, and drawn out.

Broken Stocks, Not Broken Companies

Some of the planet’s soundest companies have broken stocks. While I’m confident this is a massive opportunity for long-term investors, I’m equally certain I can’t predict the bottom.

Fortunately, I can afford a priceless weapon that most of you can too: patience.

Your personal portfolio shouldn’t be leverage. No leverage means no margin call. It’s your money. The only shareholder is you. You don’t need to “make you quarter” like the pros do on the Street. If you are in a like situation, you can afford to wait for the dust to settle, even if it means missing the first few leg of the recovery.

The market is still in good shape. And, the knockout punch (almost) never comes at the top.

Key

Macro Economic Events

Corporate Earnings

High Importance

See Note Section Below For Additional Insight

Monday

None Scheduled

Tuesday

JOLTs Report (May) | 10:00

Nike (NKE) | ATC – yes, this is the worst stock I’ve ever seen. It’s the new old-INTC. A lot going wrong, but everybody knows that.

NKE just made a 10Y low. However, they have a few things going for them.

First, the Knicks won the NBA Championship, and Nike was ready. Instead of “raffles” and “drops” that bots eat up, they’re doing pre-orders. Fans can actually get the stuff they want without having to pay up 10000000% for it on Stock X. And, there are A LOT of Knicks fans (more than their are Spurs or Thunder fans).

Second, the FIFA World Cup is in the U.S., taking place in stadiums purpose-built to sell overpriced merch and overpriced beer. Some of this money has to be finding its way into Nike’s P&L. This doesn’t even account for the extra sales from block parties with high-margin pop-ups.

Third, insider buying. Tim Cook — yes, Tim AAPL Cook — is on NKE’s board and has been loading up in the open market.

Between perfect conditions and a shift to a pre-COVID approach to distribution, I expect NKE will outperform the ground-floor expectations set by a stock price at a 10-year low.

This isn’t a broad call for a turnaround. There are plenty of structural issues NKE faces courtesy of deglobalization, but for a trade… well, I see opportunity (that will be sized appropriately small) even if it hasn’t manifested in the chart yet.

Wednesday

ADP National Employment Report (Jun) | Est. 110,000; Prior 122,000 | 08:15

Thursday

Weekly Jobless Claims (Jun 27) | Est. 221K; Prior 215K | 08:30

June Employment Report

Headline Nonfarm Payrolls | Est. 118K; Prior 172K | 08:30

Unemployment Rate | Est. 4.3%; Prior 4.3% | 08:30

Avg Hourly Earnings M/M% | Est. 0.3%; Prior 0.3% | 08:30

Avg Hourly Earnings Y/Y% | Est. 3.5%; Prior 3.5% | 08:30

Friday

Markets Closed In Observance of July 4th: Happy 250th, U.S.A