Everyone Is Wrong About Fed Hikes

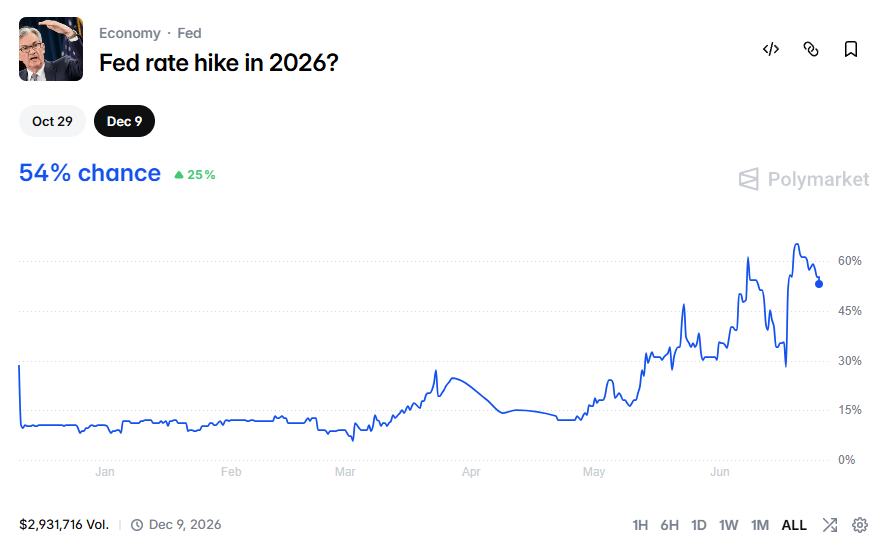

Polymarket has a 54% chance of a Fed rate hike in 2026. I’ll take the other side of that.

Walk with me.

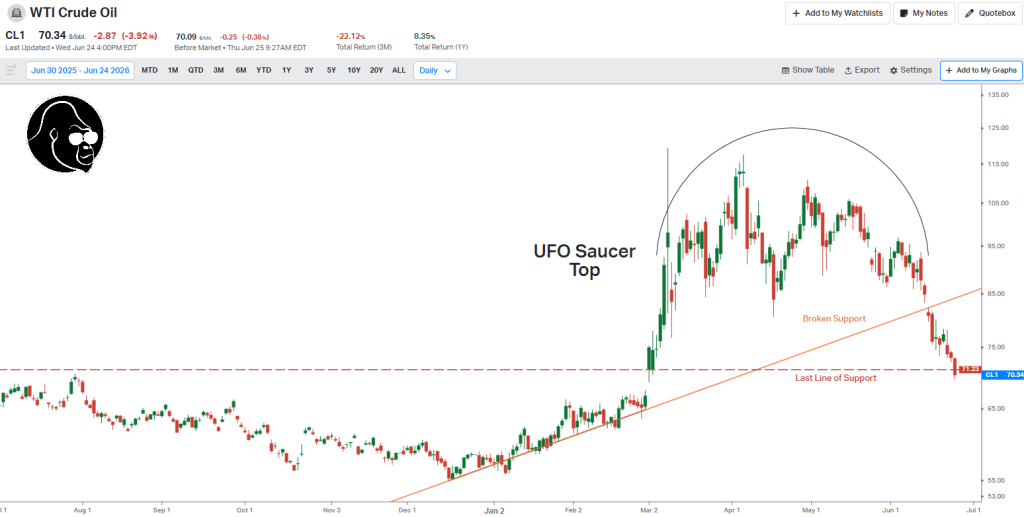

Has oil peaked?

The money says yes. If you follow me on YT, which is well worth your time, then you’d know I see WTI back to $65 before the year is out. If the money in oil is right, then investors don’t really need to worry about a Fed response to energy-inflation.

Not convinced? Fair. Single-variable analysis is doomed to fail, which is why I brought more.

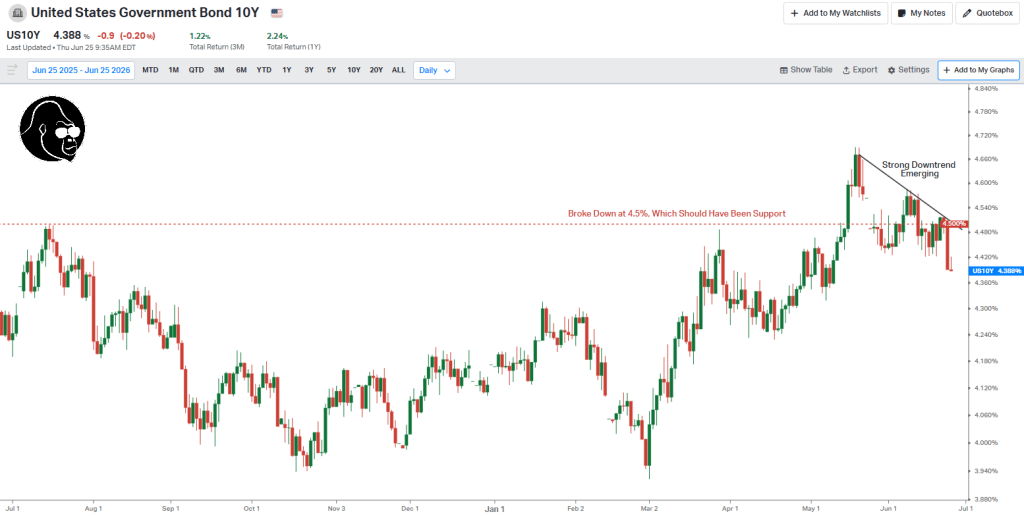

Let’s check on yields. Have yields peaked?

Seems that way. Clear downtrend is emerging, and yields collapsed where it should found support at a prior high.

But, Donny…

Don’t interrupt me.

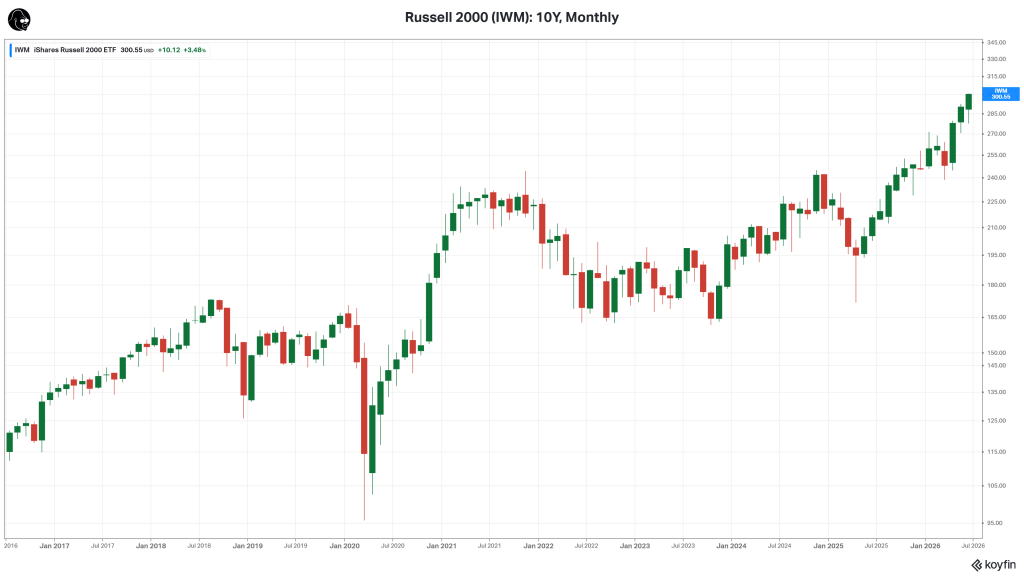

How about rate-sensitive parts of the market? The parts of the market that forget how to go up when we’re convinced we’re getting a hike?

Like the Russell 2000…

Flirting with all time highs. In fact, it appears as though this group has discovered a method to defy gravity.

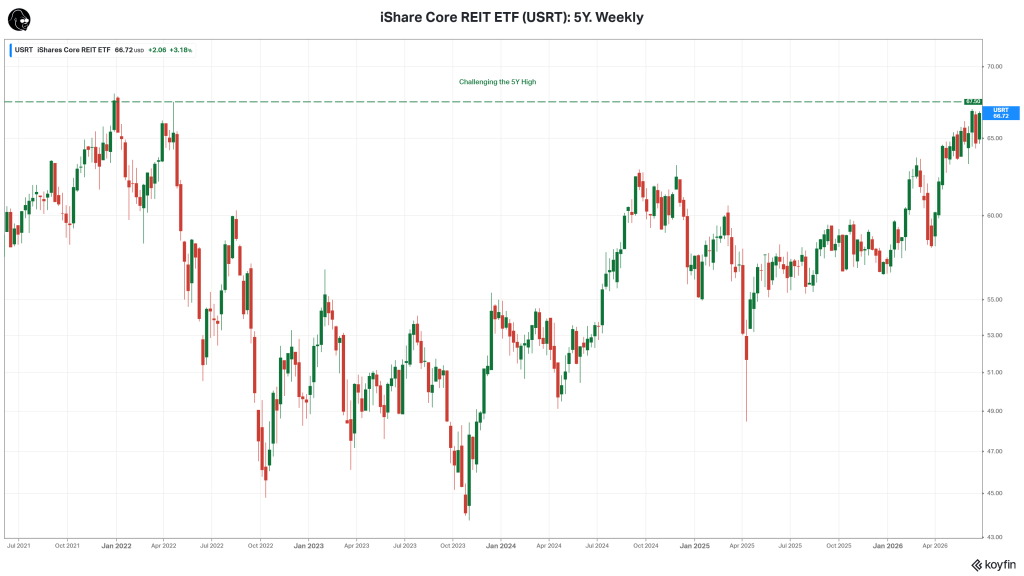

How about the REITs?

Same story, different ticker.

The money says no hike.

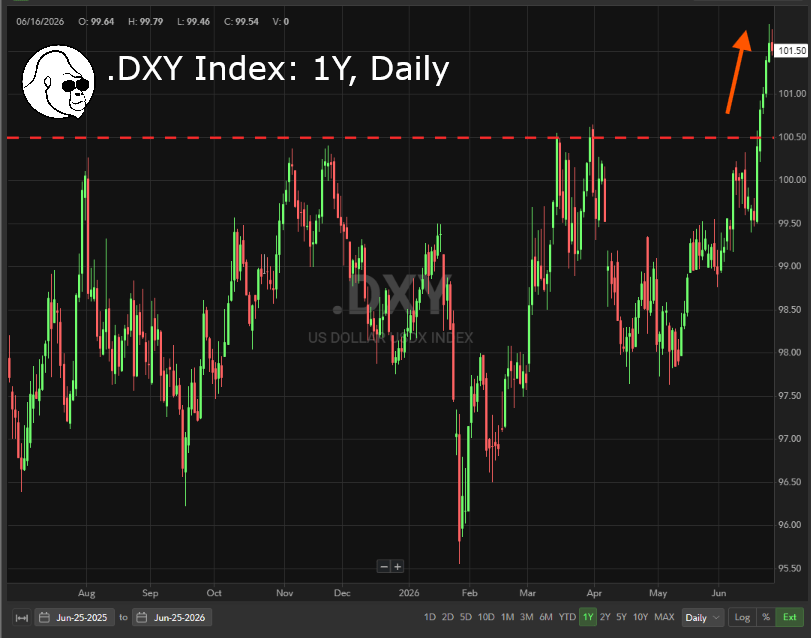

But, Donny. The USD is rallying.

The money there suggests the Fed is going to hike.

Impressive breakout. No lie. However, a different story better explains the action here.

Relative to the rest of the world, economic conditions in the U.S. are better insulated against oil-spikes. We just experienced an oil spike. If the rest of the world wasn’t on recession watch before, it certainly is now that some central banks, such as the ECB (Europe), hiked rates into the oil shock… because fighting energy inflation with rate hikes has never once worked, but sure, let’s try it again. As a result, the USD gets to play safe-haven asset until fears abroad subside.

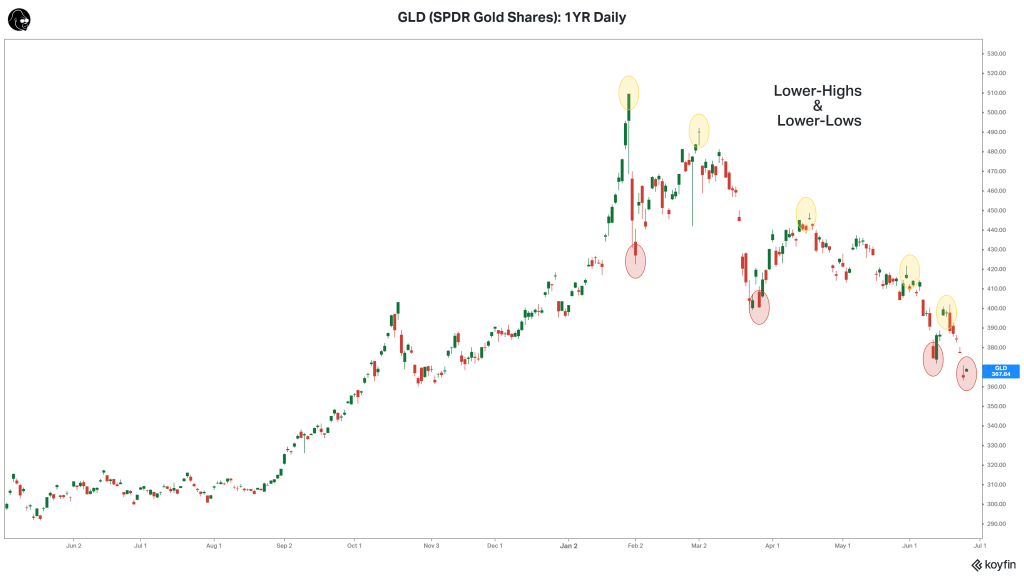

Since Russia-Ukraine, in which the dollar was weaponized against Putin, many countries have been de-dollarizing to manage the national security risk. Many of which – especially China – piled into gold, one of the few assets a central bank can hold in reserve. As this oil episode has unfolded, these central banks appear to have been net-sellers in favor of stabilizing their economies and chasing safety in the USD.

I have no idea how long this safe-bid lasts for the USD. However, I do know this: until it fades, the metals – industrial and precious – will be tough positions to hold.

Blame Warsh

I believe prediction markets are mispriced due to Warsh’s debut. Warsh knew the market would question his independence given his proximity to Trump. So he overcorrected with curt answers and hawkish rhetoric (jawboning).

Here is how I see this playing out:

Oil continues to drift and stay lower throughout the summer. The drop in oil is reflected in inflation data. However, Warsh will continue his hawkish rhetoric to maintain the Fed’s independence and keep the public’s expectations of inflation in check. This will keep prediction markets wronger for longer.

I am long prediction market contracts at an average price of 0.57 — meaning I’ll pocket 0.43 if I’m right. Yes, I bought too early, but I’m not done buying.