Warsh’s Debut Better Be Dovish

Not because lower rates would be good for stocks… but because that is what stocks are already pricing in.

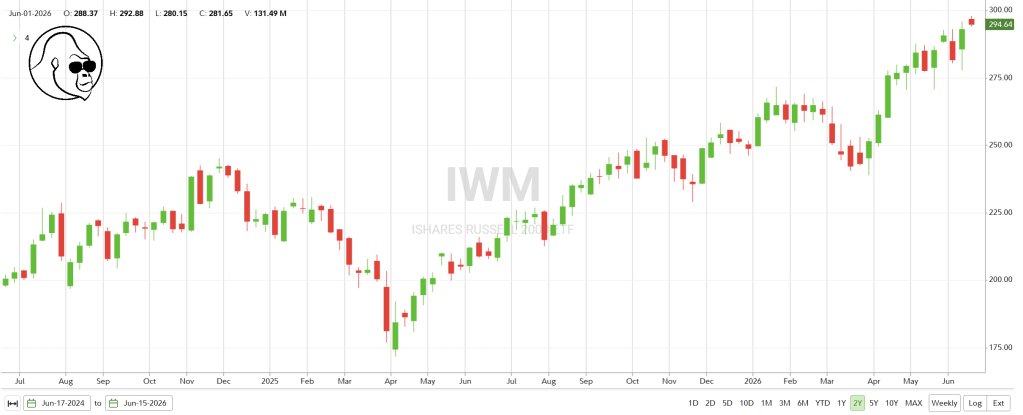

The rate-sensitive R2K — which, for years, couldn’t manage a rally without a clear path for rate cuts — is fresh off an all-time-high close. Russell 2000 names aren’t rallying in rate hike environment.

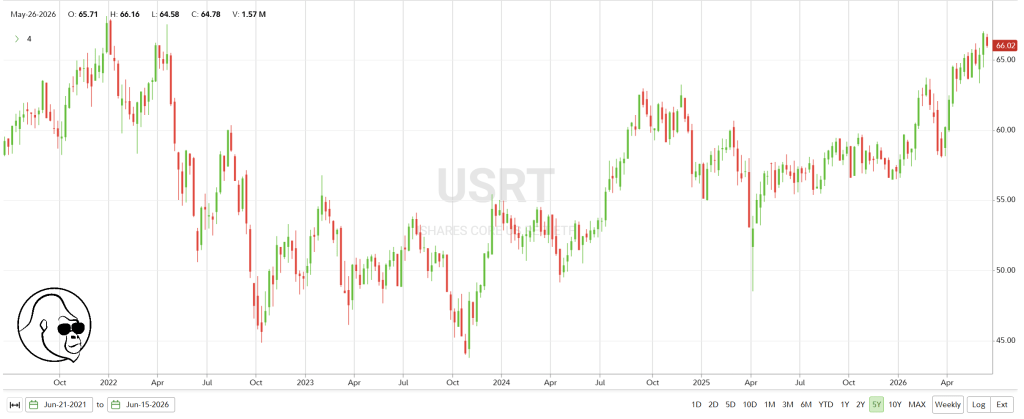

REITs, which literally compete with bonds for yield-focused dollars, is in the process of challenging a 5-year high. You don’t see REITs making these moves with the backdrop of higher interest rates.

Can Warsh Be Dovish?

In a word: yes.

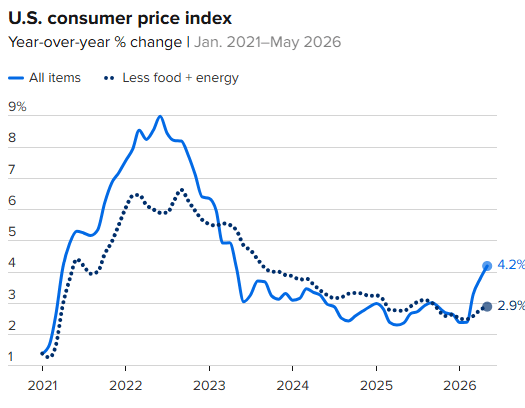

CPI inflation was hot. However, it was still within expectations. More importantly, Core CPI — which is more important to the Fed’s response function — has yet experience the same magnitude as headline. For now, the dovish argument can be made that this particular inflation flare isn’t showing signs of being sticky and is originating from a source completely insensitive to what the Fed does with short-term interest rates.

Personally, I agree with this take.

While inflation remains above target, an interest rate hike isn’t going to do anything oil prices. It will only increase the economic burden — by increasing credit car rates, car loan, etc… — for those most affected by the increase in oil and energy inputs; those in the bottom quartile of income earners; the bottom part of “K”.

Is There More Upside?

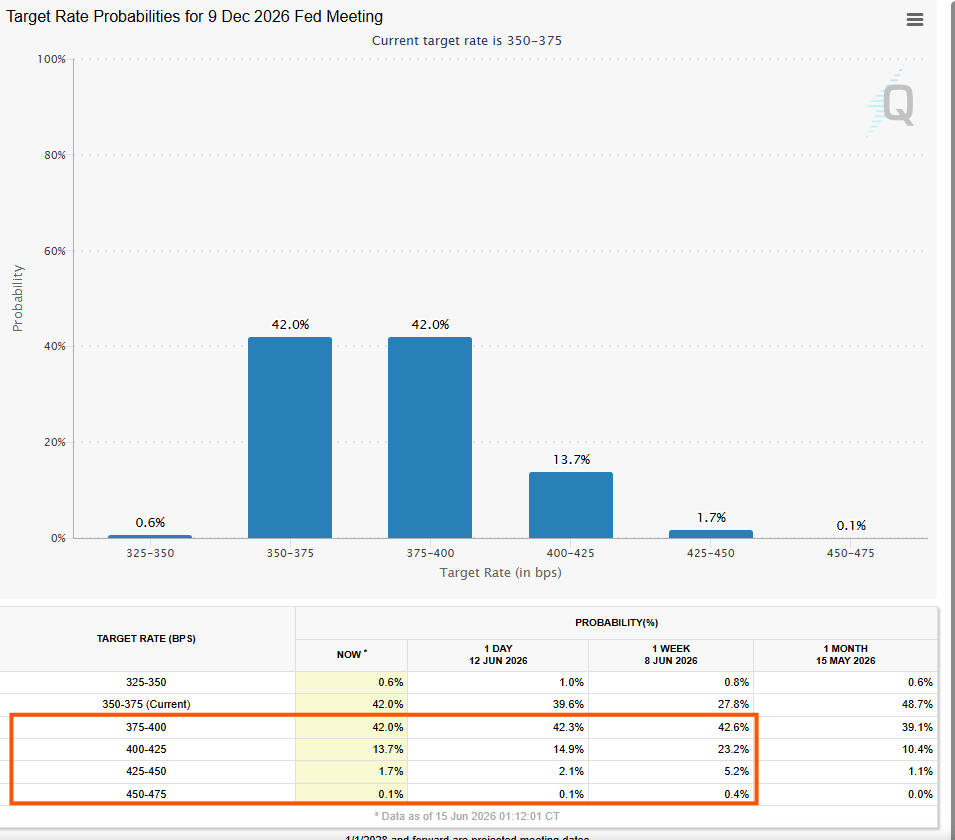

Yes. While the markets are clearly already pricing-in a dovish outcome, rate hikes are still priced-in Fed Funds Futures markets.

As those get priced out — the probabilities in the orange boxes trend toward zero — there should be more upside, most acutely in the IWM, REITs, and bonds.

If Warsh is Hawkish?

The market will have been offsides. Money will need to leave the areas of the market — which we already went over — to better reflect the economic backdrop. In such an event, I would expect the healthcare names to get a nice boost. Many of these names still trade a decent valuation relative to their growth. Growth that will to fruition regardless of what the Fed does to interest rates.