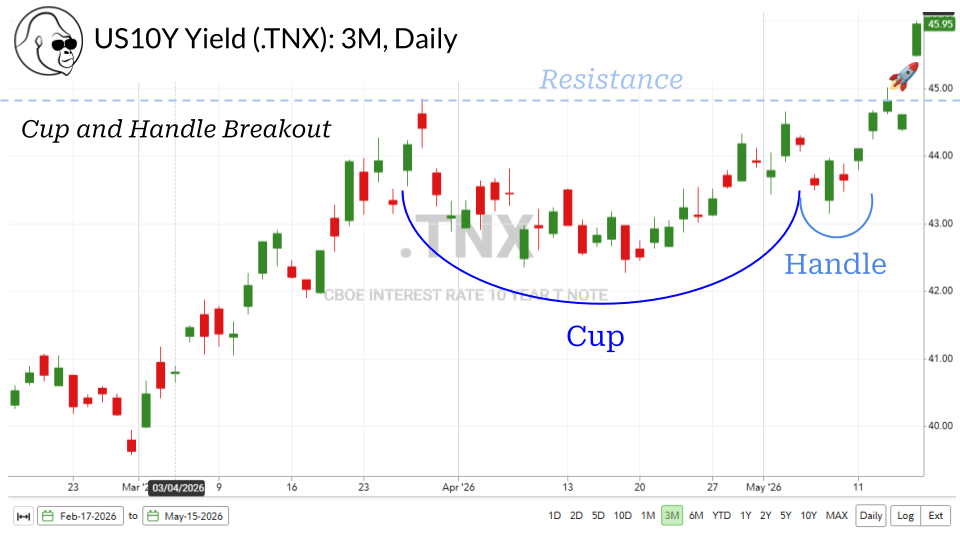

Yields Are Back

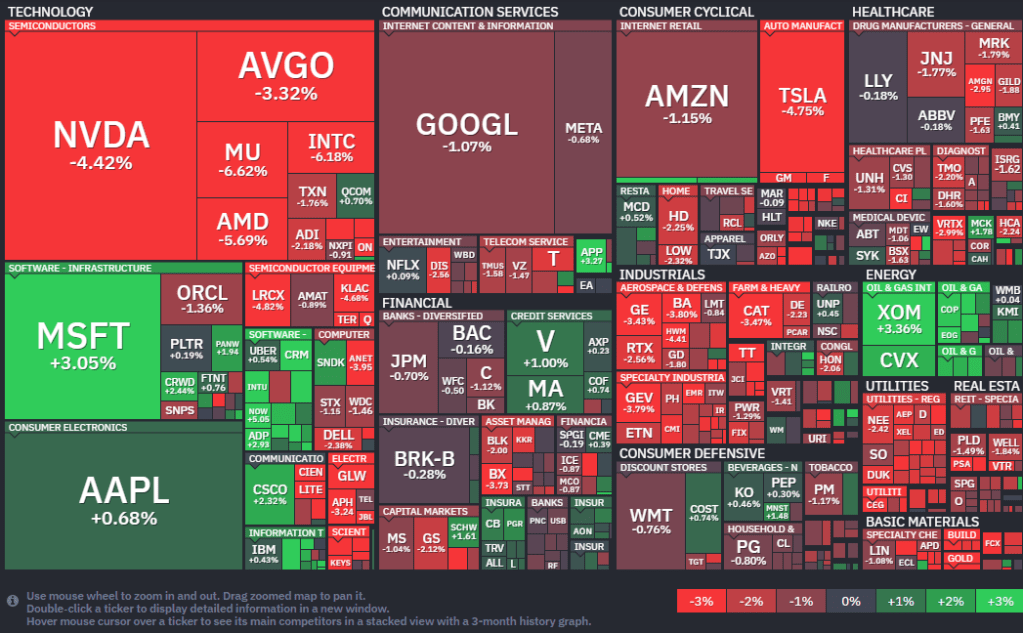

If you weren’t in the business of oil or software, Friday was a rough day for your stock. The summit between Trump and Xi failed to produce anything meaningful… which isn’t necessarily a surprise given that up to four summits are in the cards. We’re dealing with showmen. Neither Trump nor Xi would deliver anything meaningful in part one of a four-part series. That would be bad TV.

That said, the potential for China to purchase oil from the U.S. has created speculation that the arrangement is an implicit green light from China for the U.S. to restart military operations in Iran. Maybe this is what caused yields to make uncomfortable moves higher… or the bond market was anticipating a material breakthrough immediately following the summit. Without which, bonds adjusted to account for prolonged inflationary impacts associated with elevated oil prices. Either way, the result is the same: a rapid spike in yields spooked equities.

In my opinion, yields — the 10Y and 30Y — are the most important assets to watch until further notice. They’ve been the only force capable of slowing the animal spirits in the most bullish place in the markets: semiconductors.

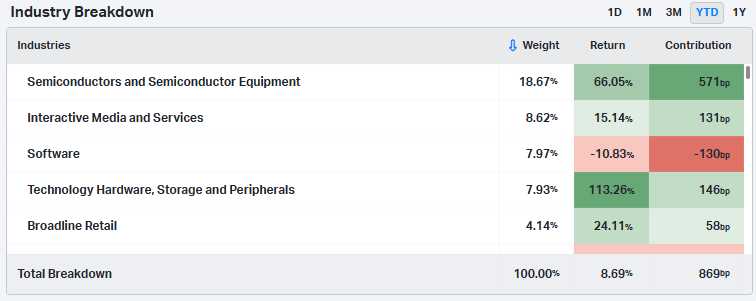

Semiconductors and semiconductor equipment are now 18.67% of the S&P 500. Ludicrous strength here has covered up ugliness elsewhere.

- 66 constituents — 13% — made a new 52W low just last week.

- 63 constituents — 12.5% — are within 10% of their 52W lows.

Even accounting for the heroic price action in semis, the S&P 500 internals resemble a bear market. Thankfully, the S&P 500 is cap-weighted; and this weakness is not present in stocks that have massive capitalizations. However… lose the semis, the door is open for the bears to come out of hibernation.

May 20th, 4:30PM

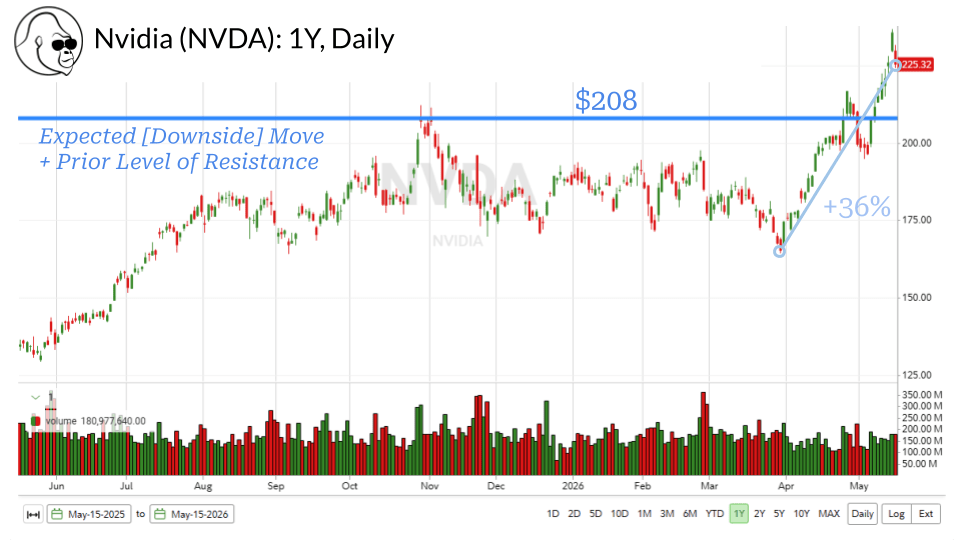

Speaking of semiconductors, Nvidia is the most important of the cohort. Sentiment is at stake here. Nvidia has the power to take the indices with it and change what has been an unrelenting bullish atmosphere around everything AI.

My podcast co-host Alvaro made the observation that Nvidia has a nasty habit of selling off after each report. I’ve noticed the same trend and actually wrote and talked about it in a prior edition of this newsletter and the podcast. This is a dangerous one to trade. You can make a lot of money trading Nvidia, but I personally would wait to do so until the quarter is in the rearview.

I like that the stock is advancing into the report. While price and expectations tend to go hand-in-hand, the expectations for this stock have been insurmountably high for the last two years. I don’t really think the recent rally changes anything.

The expected move is ∓$16.5, a little more than ∓7%. If NVDA were to experience a 7% decline – meeting the expected move – it would bring the stock back to $208. Concisely, assuming we get a reaction within the options market’s pricing, I don’t feel a lot of anxiety. Maximum damage… isn’t a lot of damage. $208 is the price it traded at on May 7th, 2026; only 2 weeks ago. It wouldn’t create a lot of bag holders and aligns with the high made last November.

I would expect buyers to assert themselves and defend $208.

Key

Macro Economic Events

Corporate Earnings

High Importance

See Note Section Below For Additional Insight

Monday

None Scheduled

Tuesday

Home Depot (HD) | BTO

Vertiv (VRT) | BTO

Toll Brothers (TOL) | ATC

Wednesday

Lowe’s (LOW) | BTO

May FOMC Meeting Minutes | 1400

Nvidia (NVDA) | ATC

Thursday

Walmart (WMT) | BTO

Initial jobless claims | Est: 210,000; Prior: 211,000 | 0830

Housing starts | Est: 1.40 million; Prior: 1.50 million | 0830

Building permits | Est: 1.38 million; Prior: 1.37 million | 0830

Philadelphia Fed manufacturing survey | Est: 18.0; Prior: 26.7 | 0830

S&P flash U.S. services PMI | Est: 51.5; Prior: 51.0 | 0945

S&P flash U.S. manufacturing PMI | Est: 53.8; Prior: 54.5 | 0945

Zoom (ZM) | ATC

Take Two Interactive (TTWO) | ATC

Friday

Consumer Sentiment (Final) | Est: 48.2; Prior: 48.2 | 1000