Believe Buffett, Not Bears

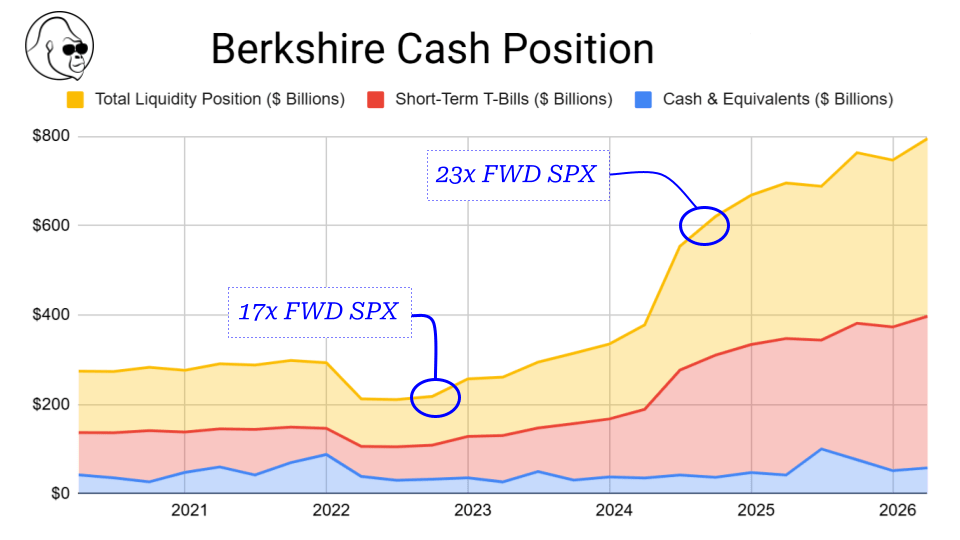

During Berkshire’s quarterly report over the weekend, the insurance conglomerate’s cash pile again rose to a new record high of $397B, up $8.1B in net equity sales.

Over the next four weeks, I expect “bear porn” to share this stat as a definitive reason to sell. Get ready for a healthy dose of this nonsense:

- “If the greatest investor of all time is this much in cash, how can you be fully invested?”

- “He knows something we don’t.”

These bears will claim this is a sudden development that warrants action. They will intentionally ignore Buffett’s consistent messaging on the matter: it is a call on valuations broadly, not a tactical move ahead of a potential crash. It is the result of Berkshire’s strategy and discipline; not fear and impulse.

As you can see, Berkshire’s cash position has been growing since the middle of 2022 and took an outsized move higher in the second quarter of 2024. In October 2022, the forward P/E on the S&P 500 troughed around 17x. By July 2024, the forward P/E was north of 23x. To the surprise of literally no one, the facts show Warren’s Berkshire raised cash as valuations rapidly rerated higher, contradicting those who claim the cash-pile is a call on an imminent crash.

Different Goals; Different Rules

Since 1999, the massive insurance conglomerate’s stated goal is to achieve an average annual rate of gain in intrinsic business value on a per-share basis. Most individuals and households are not a massive insurance conglomerate. As such, your primary goal is likely closer aligned to “compounding capital to comfortably retire,” not “preserving intrinsic value.”

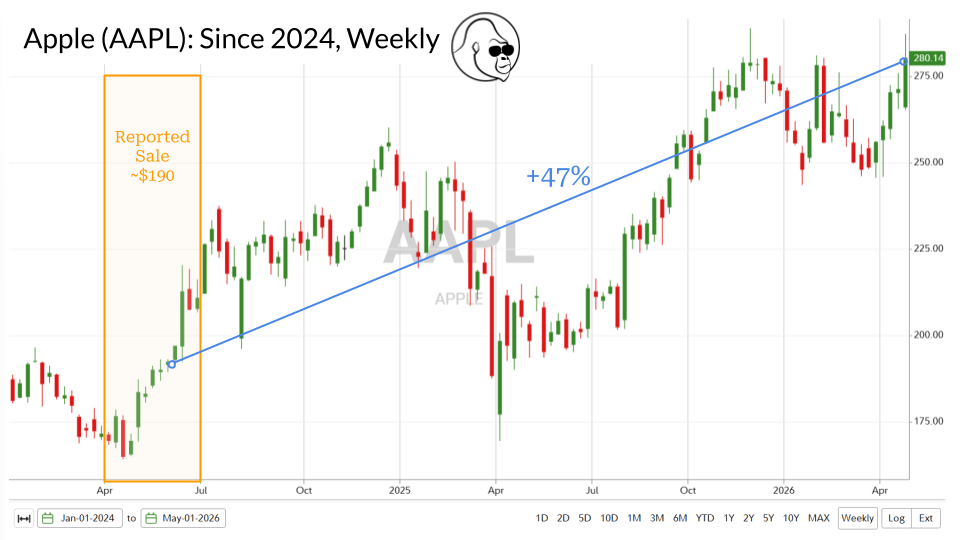

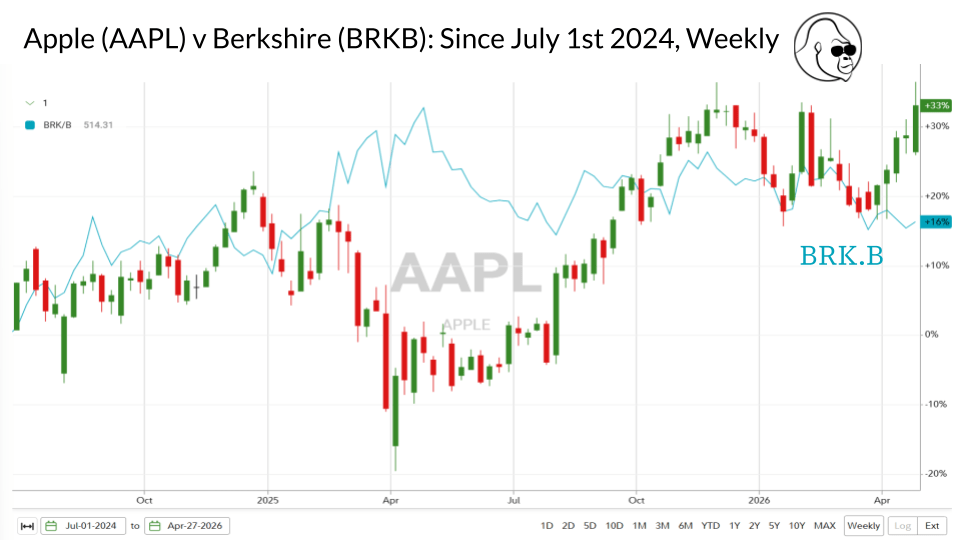

The “Buffett is Bearish” misinformation campaign went into overdrive after Berkshire’s 24Q2 report revealed a 50% sale of its largest position: Apple. Since that sale around $190 (midpoint of Q2 range), Apple has steadily clipped 47%. Adding insult to injury, since the sale, Apple has doubled Berkshire’s performance: 32% v 16%.

For Berkshire, missing that extra run in Apple (and/or the market) is irrelevant.

For you, missing that upside is of far greater consequence.

While sitting on cash may be a smart goal-oriented move for Berkshire, it may not be a smart goal-oriented move for you. Don’t let crayon-eaters on the internet convince you to follow the rules of a game you aren’t actually playing.

It’s analogous to some of the conversations surrounding the national debt. Governments carry massive debt to support programs that (hopefully) generate a social return, even if the economic return is negative. A household acting like a government would go bankrupt; conversely, an individual acting like a $900B insurance conglomerate might find themselves “safe” but “broke” relative to their retirement needs.

Key

Macro Economic Events

Corporate Earnings

High Importance

See Note Section Below For Additional Insight

Monday

Palantir (PLTR) | ATC

Tuesday

Job openings | Est: 6.8 million; Prior: 6.9 million | 1000

S&P final U.S. services PMI | Est: 51.3; Prior: 51.3 | 0945

ISM services | Est: 54.3%; Prior: 54.0% | 1000

Arista (ANET) | ATC

AMD (AMD) | ATC

Wednesday

Disney (DIS) | BTO

Uber (UBER) | BTO

ADP employment | Est: 98,000; Prior: 62,000 | 0815

IonQ (IONQ) | ATC

Arm (ARM) | ATC

Thursday

Initial jobless claims | Est: 205,000; Prior: 189,000 | 0830

U.S. productivity | Est: 1.5%; Prior: 1.8% | 0830

Coreweave (CRWV) | ATC

Friday

April’s U.S. Employment Report

- Employment report | Est: 53,000; Prior: 178,000 | 0830

- Unemployment rate | Est: 4.3%; Prior: 4.3% | 0830

- Hourly wages month over month | Est: 0.3%; Prior: 0.2% | 0830

- Hourly wages year over year | Est: 3.8%; Prior: 3.5% | 0830

May’s Consumer Sentiment (prelim) | Est: 49.5; Prior: 49.8 | 1000