I’m Making The Call

The Overton Window on $5T Stocks is Officially Open

The Overton Window:

The spectrum of ideas on public policy and social issues considered acceptable by the general public at a given time.

Think of the 4-minute mile. For decades, it was considered a physical impossibility. But the moment Roger Bannister broke it, the psychological window opened; suddenly, it wasn’t just possible, it became the new standard.

We’ve witnessed this in finance as well. $1T used to be the ceiling. Now, it’s just a sign you’ve officially made it as mega-company.

$5T is the new target.

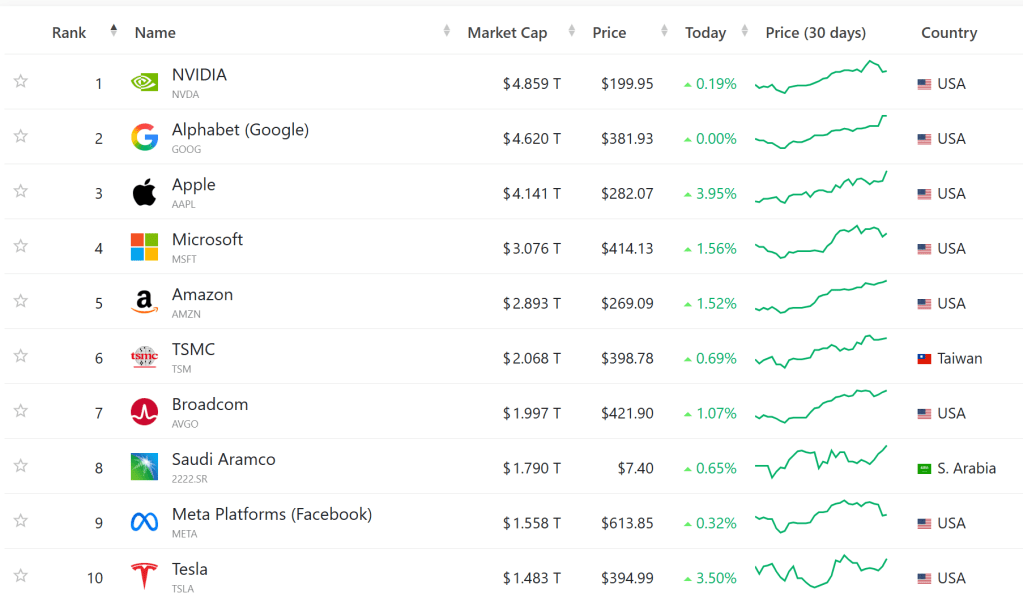

For a brief moment at the end of April, Nvidia became the first company to achieve a market capitalization of $5T… or 64,236,000 BTC for you crypto truthers out there. Now that the Mag 7 has reported – and reported well – I believe the window is open (of opportunity and of Overton) for two of these behemoths to achieve the same feat before the year ends.

No underdog story here. It’s clearly Alphabet and Apple, but for completely different reasons. Let’s start with the sexier of the two:

Alphabet (GOOG)

I won’t bore you with the numbers of the quarters; instead, I’ll give you the quote that matters:

“Gemini Enterprise is seeing tremendous momentum with 40% growth quarter-over-quarter in paid monthly active users. In subscriptions, this was our strongest quarter ever for our consumer AI plans, primarily driven by adoption of the Gemini app.”

Alphabet has succeed where Microsoft (MSFT) has failed: cross-selling their agentic agent with their cloud services. This is a legitimate return on AI investment in the form of new product innovation. These sales didn’t exist 12 months ago. Microsoft has been trying for the last two years to make Copilot into a service worth bundling with Azure… while there has been progress, the business world still views Copilot as Nopilot.

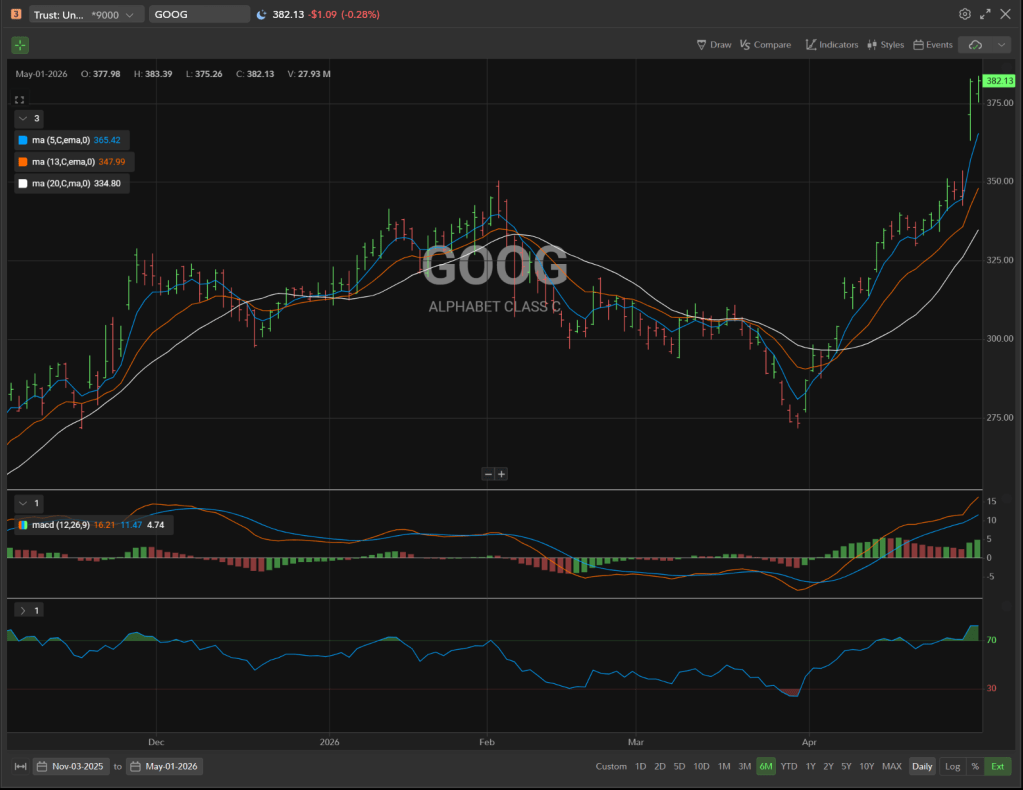

As of the time of publication, Alphabet’s market cap is $4.62T, 8.2% away from $5T. In stock price terms, ~$413.3 is the target (subject to share buybacks, etc.). Although the stock is overbought (RSI >70; bottom pane), buyers are clearly in control of this stock. There are no sellers up here in new all-time-high land. $5T seems inevitable.

If you want a little more on Alphabet’s advantage, take a moment to check out this quick clip from an episode of Charts and Checks, a weekly podcast I co-host with Alvaro of the Bilingual Stock Market Channel.

Apple (AAPL)

Perhaps you’ve heard people talk about HALO stocks?

Thank you Downtown Josh Brown for gifting the financial world the term.

Well, Apple is certainly one of them. No LLM is going to replace the iPhone, which means the recurring revenue from the service business – one of the top 3 recurring revenue streams of all time – is safe from AI disruption.

Speaking of AI, the strategy: take their cut of any subscription revenue paid to OpenAI and Anthropic transacted on the App Store. When a winner emerges, integrate that to Siri, birthing the most compelling consumer-focused AI agent ever.

Accepting a passive AI strategy is a much easier pill for investors to swallow when the underlying business continues to kick ass (that is the industry term). Success grants you both leverage and leeway, and despite oil headwinds, Apple delivered another quarter of flawless execution, further cementing the credibility of its approach:

- REVENUE: $111.18B (EST $109.66B)

- EPS: $2.01 (EST $1.96)

- IPHONE REVENUE: $56.99B (EST $56.98B)

- SERVICES REVENUE: $30.90B (EST $30.37B)

- PRODUCTS REVENUE: $80.21B (EST $79.26B)

- MAC REVENUE: $8.40B (EST $8.13B)

- IPAD REVENUE: $6.91B (EST $6.65B)

- WEARABLES, HOME & ACCESSORIES: $7.90B (EST $7.72B)

- GREATER CHINA REVENUE: $20.50B (EST $18.91B)

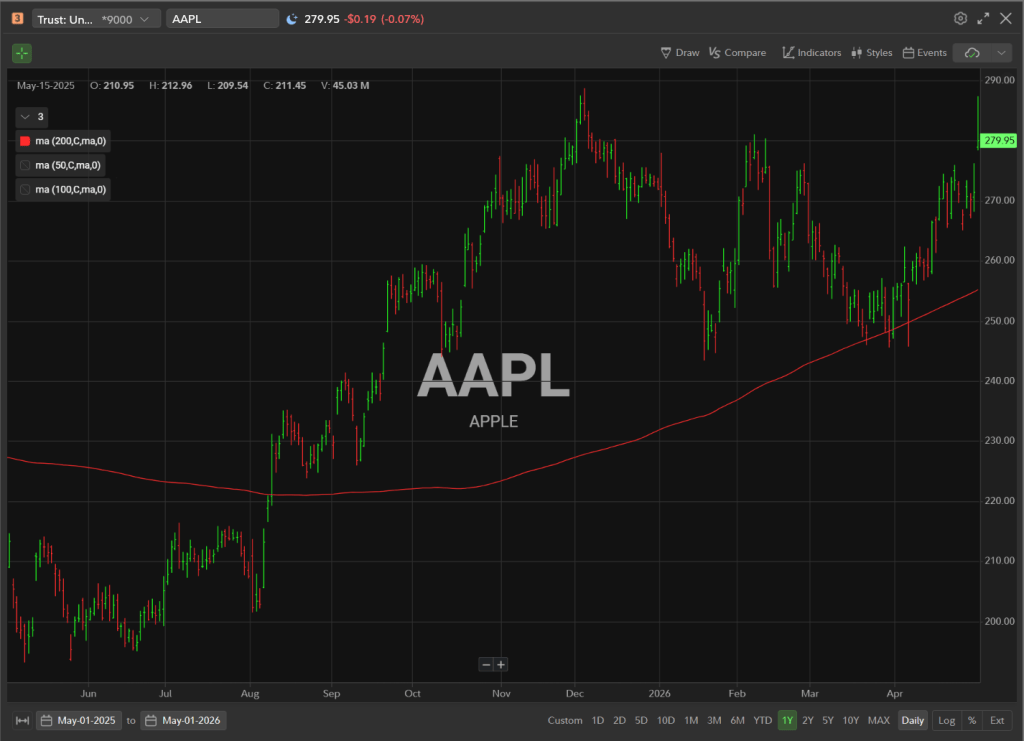

If you follow my work, you know we’ve maintained a cautious posture on Apple for some time. We initiated a starter position during the successful test of the 200-day SMA and haven’t touched it since, waiting for a catalyst. These results provide that catalyst.

My stance has officially shifted from a yellow light to a green light, meaning accumulate on pullbacks in anticipation of a retest of the ATH ~$290 and an eventual march toward the $5T milestone.

In the immediate term, watch $280. It is a PHAT number. Losing that risks filling the gap down to pre-earnings levels, which would be an excellent “pullback” to accumulate into.

Not often do you get to buy a stock that delivers a truly great report at the level it reported at.

As of the time of publication, Apple’s market cap is $4.14T, 20.7% away from $5T. In stock price terms, ~$337 is the target (subject to share buybacks, etc.).

BONUS TAKE: Meta Is Too Small

One benefit of zooming out to observe market capitalization is the simple conversation that follows: Does Company X’s size match their billing?

Take Crowdstrike (CRWD), for example: $115B seems too small for the leading cybersecurity platform in an age where data protection has never been so paramount.

Let’s Ask The Question

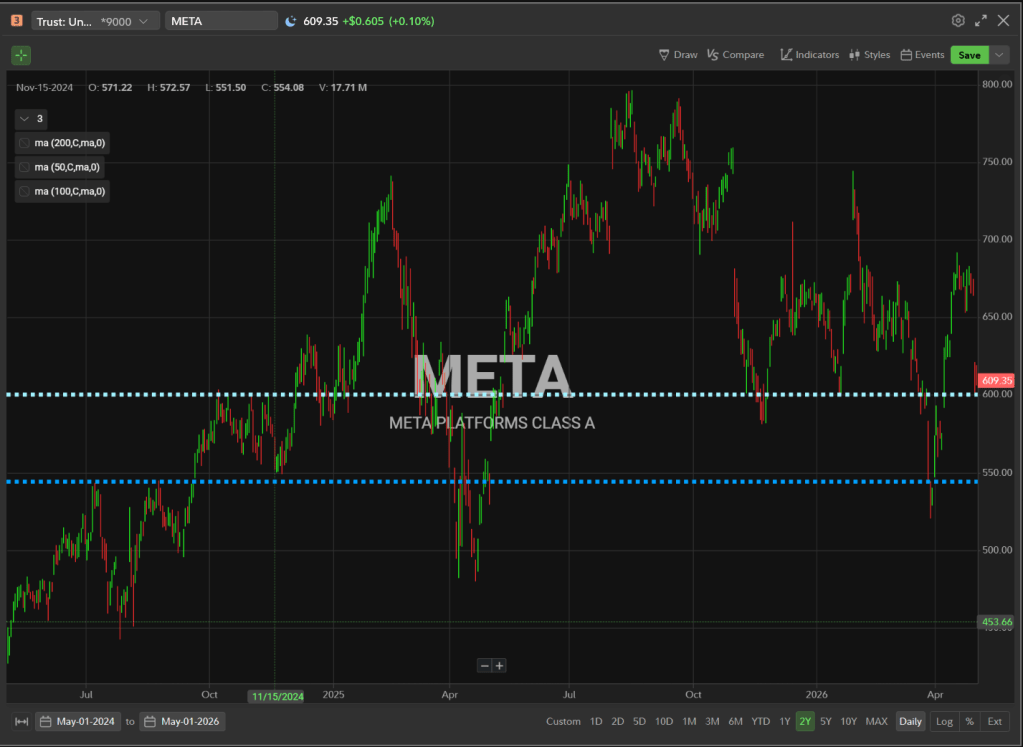

Is $1.55T too big or too small for a dominant niche in global advertising maintained/grown through one of the most ubiquitous, AI-enhanced advertising suites ever created?

Too Small.

Especially when you consider 70% of Alphabet’s revenue come from advertising…

Simple math: $4.62T * 0.7 = $3.23T

Of course, it isn’t that simple. Meta has its own problems, but shouldn’t these numbers — $3.23 and $1.55 — be closer?

Are Meta’s problems really that direr?

Simple answer: No.

I wouldn’t buy it today. Lose 600, and the next stop is 545. Bears owns the stock. Wait for some brave bulls to land a few shots first.