IGV: Nearly Full Circle

Before I get into the why, let me lay out the technical situation.

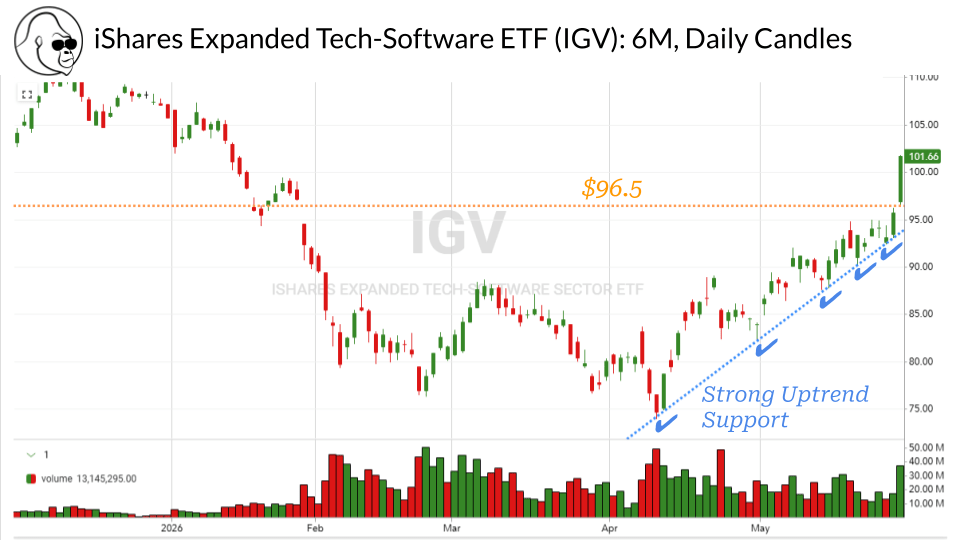

Clean breakout after consistently finding support at the bottom of a tight channel (light blue line). So long as the IGV can remain above $96.50 — the low of Friday’s breakout candle (orange line) — it makes sense to remain constructive.

The 200-day SMA is $98.84; perhaps this would be a place to look for an entry, with a convincing close below $96.50 as your stop. I have a healthy position in MSFT, so I will be looking to add exposure via trading the IGV. If I were to do so, I would actually look to do so after a retest of that $96.50 level.

And we have Snowflake (SNOW) and Okta (OKTA) to thank for it — though they didn’t do all the work.

Fortinet (FTNT) landed a decisive blow by landing a major deal to provide cybersecurity for an “unnamed infrastructure provider” building AI compute. This substantial, concrete example of AI resulting in higher (not lower) demand for high-margin software solutions cleared the path for amazing results from SNOW and OKTA to put a dagger in the SaaS-pocalypse thesis. In fact, I think we’re inches from coming full circle on the relationship between AI and software.

AI will revolutionize software companies, not end them.

In my opinion, what the market got wrong was identifying software’s only moat as its code. People convinced themselves that vibe-coded solutions were a valid substitute for all expert software solutions. It turns out, many of the world’s most important software companies are more than just their code. Of course, the code matters, but software companies provide value through their expertise, platforms, relationships, and more.

This is not a green light to buy all software.

Software companies that fail to justify their worth beyond their code — low stakes items, non-mission critical services, etc… — remain in jeopardy. When the tide falls, I expect this brand of software to follow suit. However, the notion that software was facing an extinction level event has clearly lost steam, and it isn’t too late to invest in some winners that will ride beyond the tide.

This will look obvious in hindsight, but if you look through the lens of the Gorilla with Glasses, you wouldn’t need hindsight to see 20/20. You have been on the right side of this the whole time.

Key

Macro Economic Events

Corporate Earnings

High Importance

See Note Section Below For Additional Insight

Monday

S&P Final U.S. Manufacturing PMI (May) | Prior: 55.3 | 09:45

ISM Manufacturing (May) | Est: 53.2%; Prior: 52.7% | 10:00

Construction Spending (April) | Est: 0.3%; Prior: 0.6% | 10:00

Tuesday

Dollar General (DG) | BTO

Cleveland Fed President Beth Hammack Speech | 08:55

Job Openings (April) | Est: 6.9M; Prior: 6.9M | 10:00

Palo Alto Networks (PANW) | ATC

Wednesday

ADP Employment (May) | Est: 120,000; Prior: 109,000 | 08:15

Federal Reserve Governor Michael Barr Speech | 09:00

S&P Final U.S. Services PMI (May) | Prior: 50.9 | 09:45

Factory Orders (April) | Est: 4.3%; Prior: 1.5% | 10:00

ISM Services (May) | Est: 53.9%; Prior: 53.6% | 10:00

Fed Beige Book | 14:00

Broadcom (AVGO) | ATC

CrowdStrike (CRWD) | ATC

Five Below (FIVE) | ATC

Veeva Systems (VEEV) | ATC

Thursday

Initial Jobless Claims (May 30) | Est: 215,000; Prior: 215,000 | 08:30

U.S. Productivity (Q1) | Est: 0.6%; Prior: 0.8% | 08:30

ServiceTitan (TTAN) | ATC

Friday

May Employment Report

Nonfarm Payrolls | Est: 90,000; Prior: 115,000 | 08:30

Unemployment Rate | Est: 4.3%; Prior: 4.3% | 08:30

U.S. Hourly Wages | Est: 0.3%; Prior: 0.2% | 08:30

Hourly Wages Year-over-Year | Est: 3.4%; Prior: 3.6% | 08:30

Consumer Credit (April) | Est: $18.0B; Prior: $24.8B | 15:00