Matters of Fundamentals

Despite serving a 3-Star Michelin quarter, Nvidia shareholders sent it back.

- EPS: $1.62 adjusted vs. $1.53 estimated (+5.9%).

- Revenue: $68.13B vs. $66.21B estimated (+2.9%).

- Revenue Guidance: $78B vs. $72.6B estimated (+7.4%).

At $180, Nvidia is trading at 21.8x FWD (12 months) earnings, anticipating 73.17% YoY EPS growth. The growth more than justifies this valuation. It isn’t expensive compared to the S&P 500 either. Currently, the benchmark index is trading around 21.9x FWD, anticipating 14.7% YoY EPS growth (as per FactSet, page 17).

Matters of Multiples

If you have eyes and ears, you can’t claim it is the fundamentals or execution. That leaves matters of the multiple. So, better question: why is the multiple (or valuation) compressing? What bearish outcome is the market attempting to price-in?

Could it be competition from TPUs?

I understand that 50% of AVGO’s revenue is derived from the sinful revenue stream that is software – may as well not even report it honestly – but this chart shouldn’t look this sorry if TPUs were to blame for NVDA’s malaise.

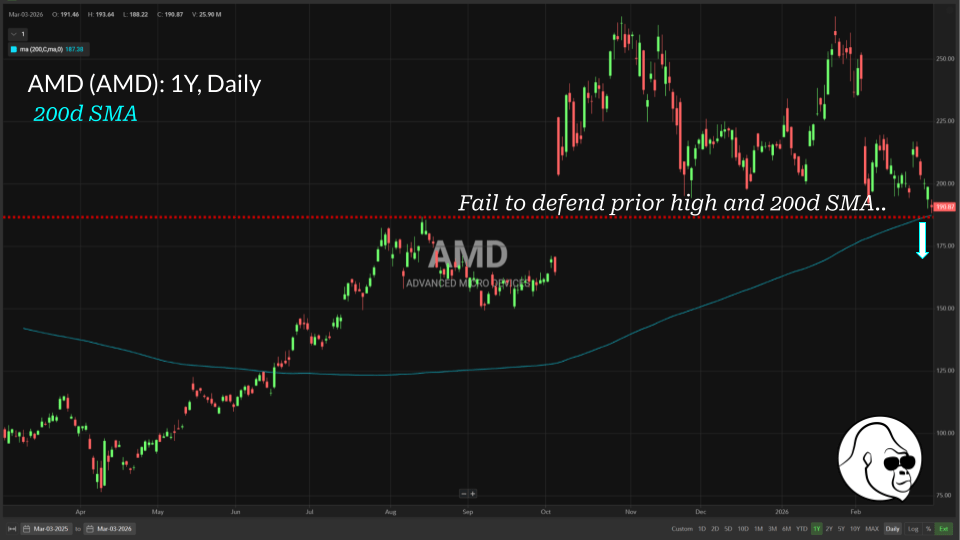

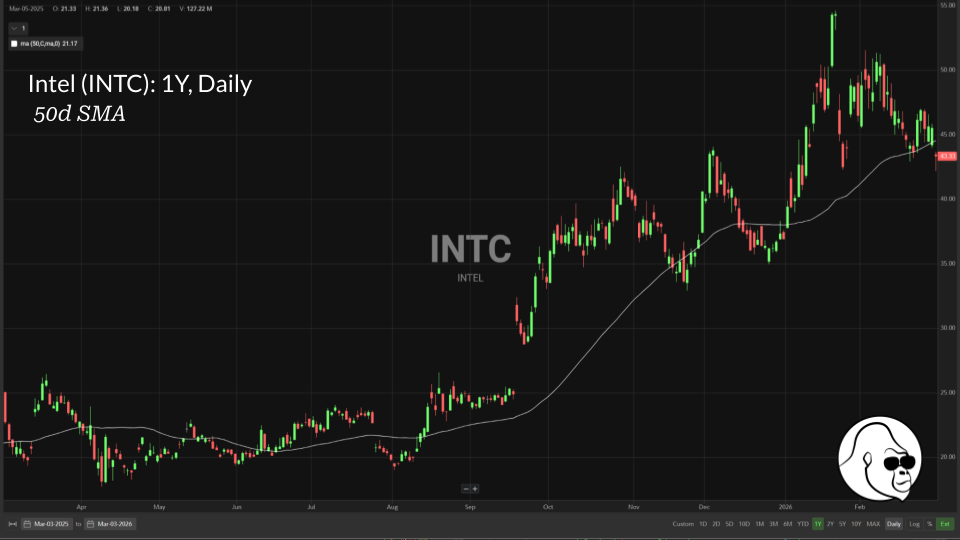

Could it be hyperscaler GPU diversification via AMD and INTC?

Not as bad as AVGO, but not as good as Nvidia, frankly. Why bother sharing this with you… well, these examples brought me to the following conclusion:

Nvidia’s problem isn’t an Nvidia problem; it is a GPU problem.

Circular Financing…

… has been a concern for some time now.

My best guess as to the market’s decision to let Nvidia trade at a discount relative to its growth and the S&P 500 is an attempt to price-in some amount of “bad revenue”: orders in their guidance that do not get fulfilled.

Put another way, if OpenAI or Anthropic cannot follow through on all their financial commitments, how much of Nvidia’s (and INTC, AMD, AVGO, etc…) revenue guidance falls through too?

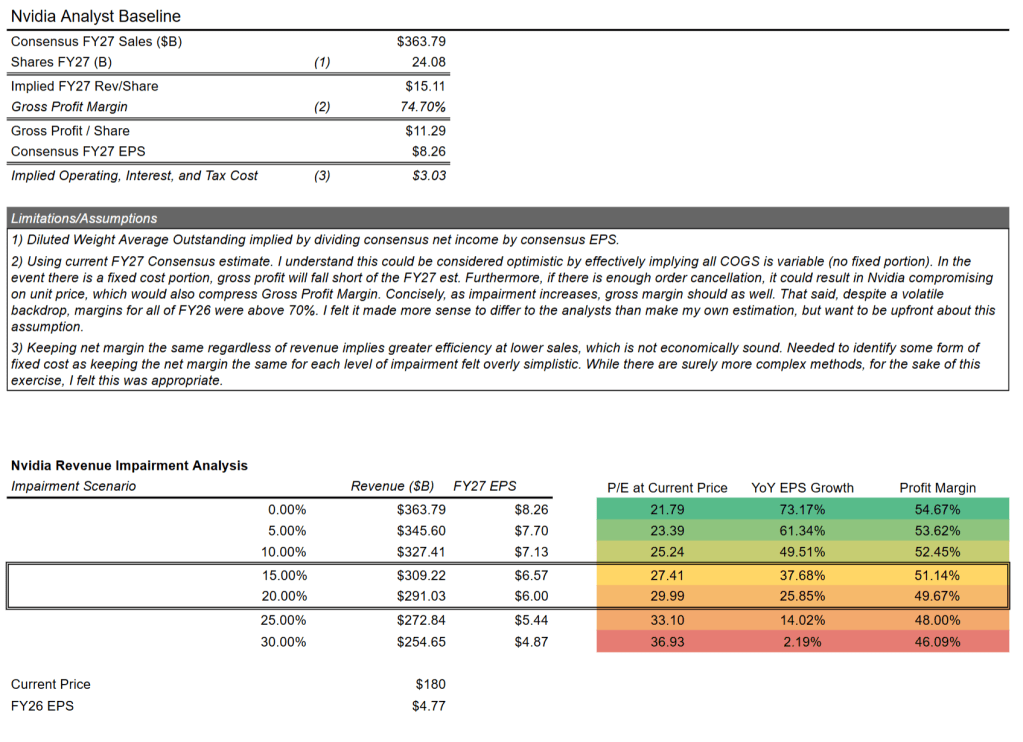

Based on my model, an impairment of 15-20% of NVDA’s total revenue would be necessary before Nvidia is expensive relative to its growth. At this threshold and a price of $180, the YoY EPS growth would exceed the forward Price-to-Earnings (P/E) ratio, which many textbooks would assert is a sign that a stock is overpriced. This analysis, as I detail below, is subject to certain limitations.

Here’s a .cvs link to my analysis. Feel free to play around with it and come to your own conclusions. You can click on the button below to see the full analysis.

But, in a world where 15-20% of Nvidia’s orders fall through, I’d argue there is plenty of demand waiting for the opportunity to jump ahead of their current space in the GPU-queue. On their most recent quarterly call, CFO Colette Kress stated that Nvidia has inventory and supply commitments in place to address demand extending into calendar 2027.

The demand is there. Any cancelled orders will be quickly reallocated.

Matters of Size

At the end of the day, stock prices move on supply and demand just like anything else.

At $4.4T in market cap, perhaps there simply isn’t enough incremental capital to force Nvidia higher. To put it into perspective, Nvidia’s market cap currently rivals Japan’s GDP at ~$4.46T and India’s at ~$4.5T. Nvidia is currently larger than S&P 500 Consumer Staples – worth approximately $4.1T – and the S&P 500 Materials – worth approximately $3.2T.

Another factor working against the stock are alternative investment opportunities. While I find Nvidia’s valuation and growth compelling (and don’t buy the bear thesis), there is no denying that there are other trades working across sectors, market caps, and geographies that have gone overlooked and underinvested.

Although the breather in the name has been long, I don’t view it as a negative. In fact, you can make the argument the prolonged pause in Nvidia has allowed for market breadth to fill in, which isn’t a bad thing for those who aren’t 100% invested in tech.