Weekly Performance

| S&P 500 | 1.82% |

| Equal Weight S&P 500 (RSP) | 2.49% |

| NASDAQ | 1.69% |

| DOW | 2.71% |

| Russell 2000 | 3.40% |

Talk of the Tape

Although ADP posted a negative headline number, Payrolls didn’t show the same softness. While some details suggest the headline strength in Payrolls may be overstated, the drop in unemployment to 4.1% from 4.3% all but eliminates the likelihood of a rate cut before September.

The Week Ahead

Monday

- n/a

Tuesday

- n/a

Wednesday

- FOMC Minutes

- Tariff Deadline

Thursday

- Initial Claims

Friday

- n/a

Macro Movers

Single Variable Analysis – June Payrolls

There was some quick debate as many scrambled to get an early start to their July 4th holiday over whether the Payrolls report was as strong as the headline suggested. For those keeping score at home, here were the key metrics:

- Headline Payrolls: 147k actual vs. 110k estimate and 144k prior

- Annual Average Hourly Wages: 3.7% actual vs. 3.9% estimate and 3.8% prior

- Monthly Average Hourly Wages: 0.2% actual vs. 0.3% estimate and 0.4% prior

- Unemployment Rate: 4.1% actual vs. 4.3% estimate and 4.2% prior

In my view, unemployment moving back toward 4% was the single most important line. It really can’t be overstated. So I’ll keep finding slightly different ways to say the same thing: as long as Americans have jobs, betting on a recession is a bad bet. The risk-on reception — gold down, yields up, stocks up — suggests the market took this Payrolls report as non-recessionary. For the Fed, it provides cover to remain on hold through the summer.

July 9th – Tariff Deadline

Just because Payrolls put recession-watch on hold for 30 days doesn’t mean stocks are invulnerable to a pullback. The S&P 500 is at a new all-time high, trading at 24x trailing and 23x forward earnings. It’s a bit rich, suggesting the market has priced in a combination of successful trade deals/frameworks and an extension of the current tariff pause for those negotiating in good faith ahead of the Wednesday, July 9th deadline.

With little in the way of economic data or earnings this week, trade developments will dominate the narrative. Otherwise, the only foreseeable landmine is initial claims. That said, if we do get some jitters (this week or through the month), I believe the non-recessionary Payrolls report gives investors permission to buy dips and maintain a bullish bias.

Initial Jobless Claims

- Expectations are for 235k, effectively flat compared to last week’s 233k.

Micro Movers

Follow-Up: The Averages Must Confirm Each Other

There aren’t any companies reporting this week that I’ll be watching closely or know well enough to comment on. However, last week’s close brought further confirmation of the S&P 500’s new high via the equal-weight index (RSP), led by continued strength from emerging leadership in the industrials and financials sectors.

Paired with the broader risk-on reaction to the Payrolls report, strength in industrials and financials reinforces the message that the U.S. economy is not trending toward recession. With XLF printing a new all-time high, the space is ripe for breakouts.

The passage of the “big beautiful bill” — regardless of your personal views on its content — has served as a positive catalyst for the market, removing the overhang of a broader government shutdown or the potential repeal of favorable tax rates.

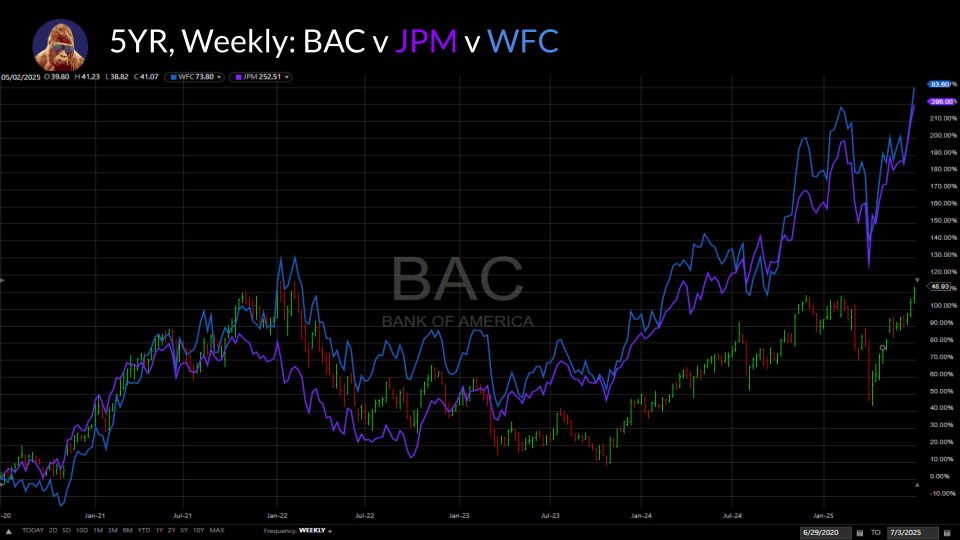

So, to cap off this week’s brief, here’s something actionable for Bank of America (BAC).

Since the pandemic, BAC has underperformed both JPM and Wells Fargo (WFC) since coming out of the pandemic. JPM stands head and shoulders above the rest of the group, but the performance gap between BAC and WFC feels a bit extreme. With the XLF making a new high, I believe there is a window for BAC to narrow that gap. If you want to play this, you’ve got a few options.

Quick Disclaimer: I am long BAC. Along with JPM, BAC is a core position that provides my portfolio exposure to the financial sector. I am not currently executing the strategies I am about to outline below. I am simply laying out how I would approach a trade in BAC.

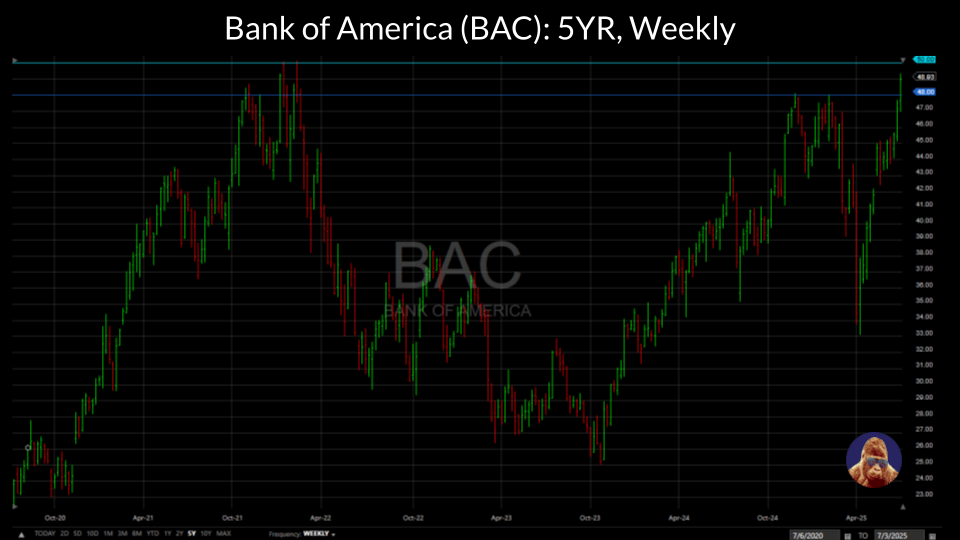

Option 1: Wait for the Breakout

If BAC breaks above $50, just buy it. There aren’t any sellers at $51. I don’t believe in triple tops. If BAC punches through, it’ll run. To the upside, I’d use a weekly close below the 5-day EMA.

Option 2: Buy Now

You could pull the trigger tomorrow and set a stop-loss on a convincing close below $47–48. If bulls lose control of that level, it could suggest a bigger catalyst is needed. Assuming the breakout comes, you’d then apply the same 5-day EMA rule as outlined in the prior setup.

Option 3: Play the Earnings

Speaking of catalysts, BAC reports on July 16th (next Wednesday). You could wait for the report or play it with options near the $50 strike. Of course, if BAC doesn’t break out, those will expire worthless.

Typically, I don’t highlight options-based trades, but this setup offers a unique benefit: clearly defined risk ahead of anticipated (earnings) volatility. The most you can lose is the premium paid. That’s a known risk. Owning shares into earnings, especially if you’ve committed to a position of size, could lead to a larger single-day dollar loss in the event a disappointing report gaps the stock materially lower.

If you’re still here and liked what you read, could you do me a favor? Consider subscribing to my website by signing up below for insights delivered directly to your inbox. If that doesn’t suit your fancy, consider dropping me a follow on LinkedIn, or sharing my work. Thank you for reading.