Weekly Performance

| S&P 500 | 3.06% |

| Equal Weight S&P 500 (RSP) | 2.16% |

| NASDAQ | 3.99% |

| DOW | 3.58% |

| Russell 2000 | 2.97% |

Talk of the Tape

Despite a late-session decline on reports that U.S.-Canada trade talks had fallen apart, the S&P 500 and NASDAQ found their footing, achieving new all-time closing highs.

The Week Ahead

Monday

- n/a

Tuesday

- JOLTs

Wednesday

- ADP Employment

Thursday

- June Payrolls

- Initial Claims

Friday

- Markets Closed: 4th of July

Macro Movers

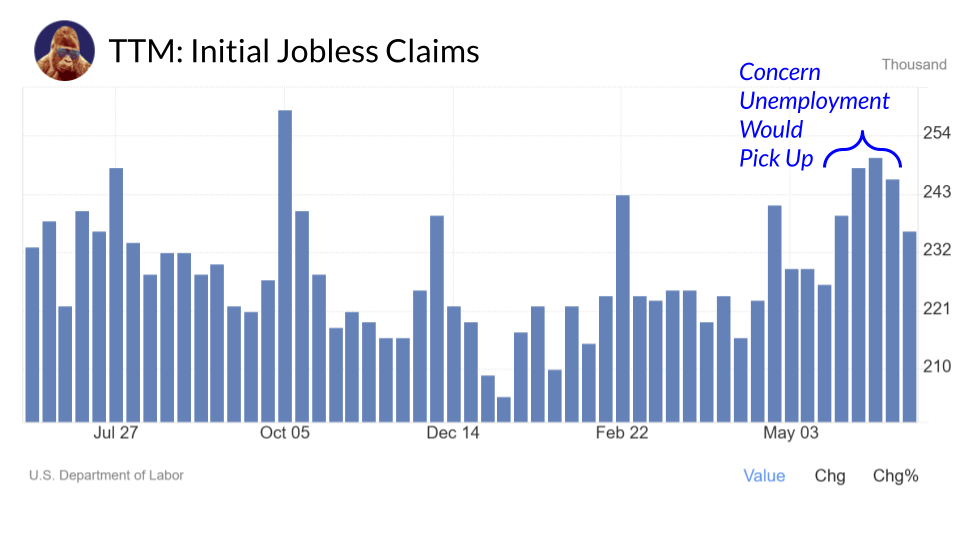

Labor Market Confirmation

This is our first look at data for June. Last week, initial claims backed off a touch, which left everyone in an incremental better mode.

Due to the Fed’s insistence on a prolonged hold in light of potential tariff-driven inflation, we need the labor data to — again — provide confirmation that the Fed has the luxury of patience by showcasing a resilient job market.

JOLTs (May)

- Within JOLTs is job openings. Although the data is for May, the consensus is 7.3 million. In April, this metric came in at 7.4 million. A meet or beat would back the Fed’s patient stance.

ADP Employment

- Private sector job creation is expected to rebound from last month’s concerning 37k. Consensus forecast is set at 120k. An upside surprise would support the notion the economy is fine at the current level of rates.

Initial Jobless Claims

- Last week’s 236k was a welcome downside print. This week, the forecast is set at 240k. So long as the data doesn’t suggest we’ll start seeing this series move toward 300k, this shouldn’t do much for the market, especially considering Payrolls will release the same morning.

Payrolls (June)

Money metrics are headline job creation, unemployment, and average wages. With respect to price action, I view unemployment as the most important. Hard to argue earnings are at risk so long as the population is employed. As such, we want unemployment to meet or come in below the estimate.

At the same time, similar to ADP, we’ll be looking for job creation to beat or meet.

As for average wages, we just don’t want these numbers to stray too far from the estimates. The Fed has signaled they believe the only potential source of inflation in this economy is tariffs. We don’t want to see the labor market return as an inflation risk factor.

- Headline job creation is expected to print 115k, slightly off last month’s 139k.

- Unemployment is expected to tick up by a tenth to 4.3% from 4.2%.

- MoM average wages are projected to rise by 0.3%, a tenth lower than 0.4% the prior month.

- YoY average wages are projected to remain at 3.9%, same as last month.

Micro Movers

In the absence of any major earnings reports and in the spirit of fresh highs on the S&P 500 and NASDAQ, I thought it an opportune moment to share a few charts that lend credibility to these breakouts and help pick some winners.

Quick Disclaimer: the jobs data has the influence to alter the market conditions that have powered this run from the April low. If the data suggests the economy — and by extension, earnings — are at risk, these all-time highs won’t prove durable. But if the labor data doesn’t upset the current narrative, then what I lay out below becomes the conversation.

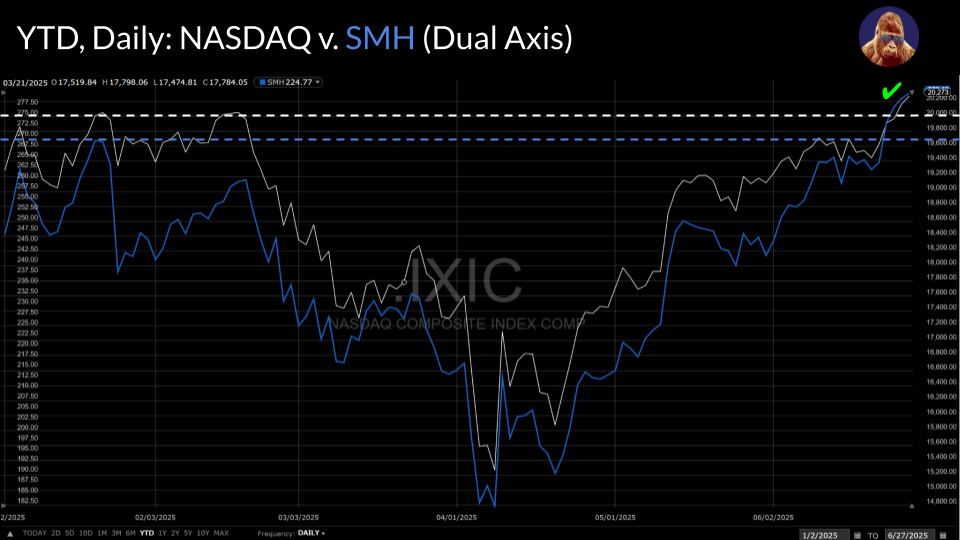

The Averages Must Confirm Each Other

Dow Theory holds that a new high in the Dow Industrials (DJI) must be confirmed by a new high in the Dow Transports (DJT) to be considered durable. The principle dates back to the early 1900s. The economy is different now, but the logic still applies.

Personally, I view semiconductors, as tracked by the SMH, as the new Transports. Given the NASDAQ’s ~20% exposure to semis, I believe it is fair to use the SMH as a confirming average. In this case, the highs confirm each other. That’s a strong signal.

Within the SMH, several leaders have made not only new 52W highs, but fresh all-time highs (ATH): Nvidia (NVDA), Broadcom (AVGO), and Taiwan Semiconductor (TSM). The SMH is rich with opportunities for stock-pickers. Even the semiconductor equipment makers (AMAT, ASML) are showing signs of life after having endured a nearly 11-month downtrend dating back to last July.

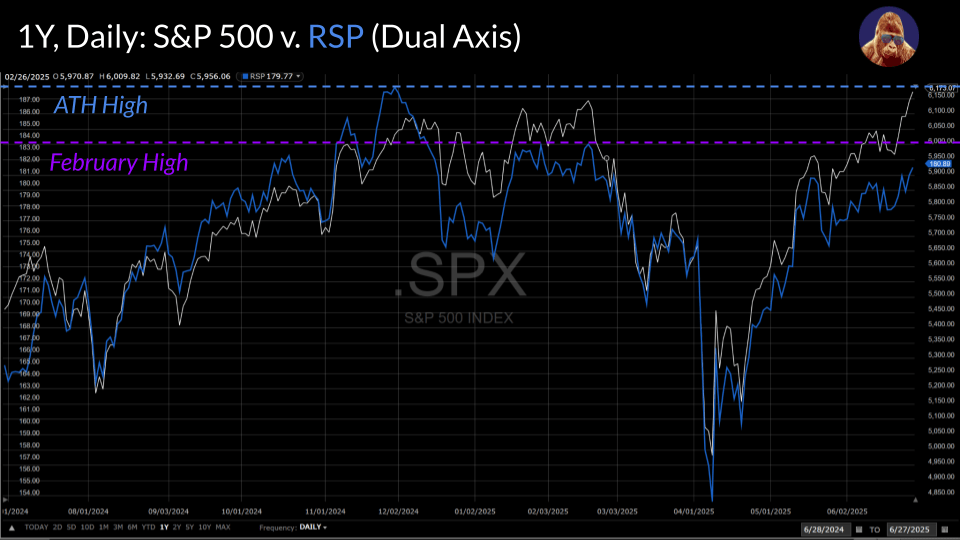

The S&P 500 is a bit more nuanced. I like to use the equal-weight version, the RSP, for confirmation. Clearing the ATH, about 4% away, would be a masterpiece. That said, convincingly clearing February’s level — ~$184, ~1% away — would be an undeniable indication of strong breadth, which we all look for to feel good about new highs. Concisely, as of Friday’s close, the case S&P 500 confirmation is not as strong as that for the NASDAQ.

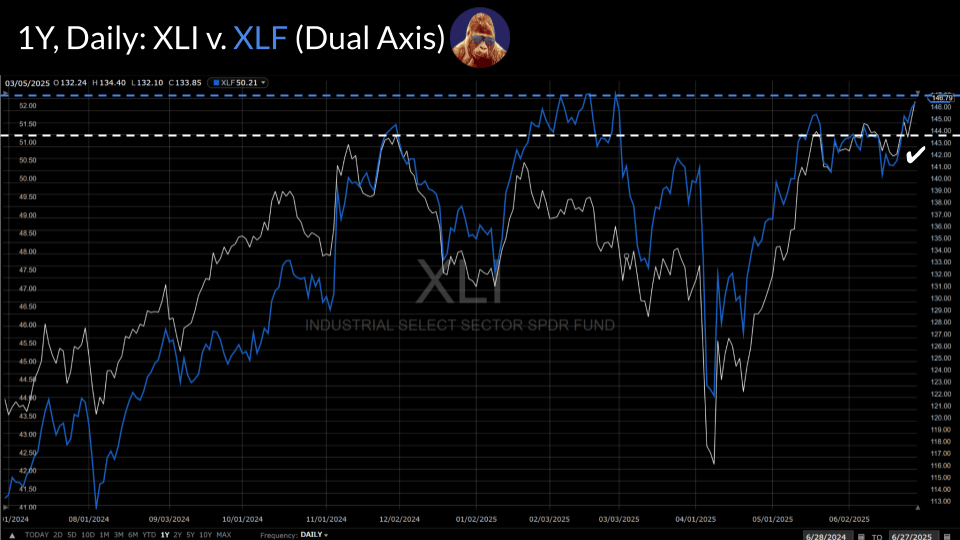

That said, you can also look to certain S&P 500 sector ETFs to confirm a new high in the broader index. Getting confirmation from cyclical sectors — like say the industrials (XLI) and financials (XLF) — is considered a fairly strong endorsement because the market wouldn’t bid up these sectors if there were legitimate concerns surrounding the economy.

We have confirmation already from industrials (XLI). As for the industrials, I am newly long Jacobs (J) and Boeing (BA). The former is still in the accumulation phase; the latter is in the participation (momentum) phase.

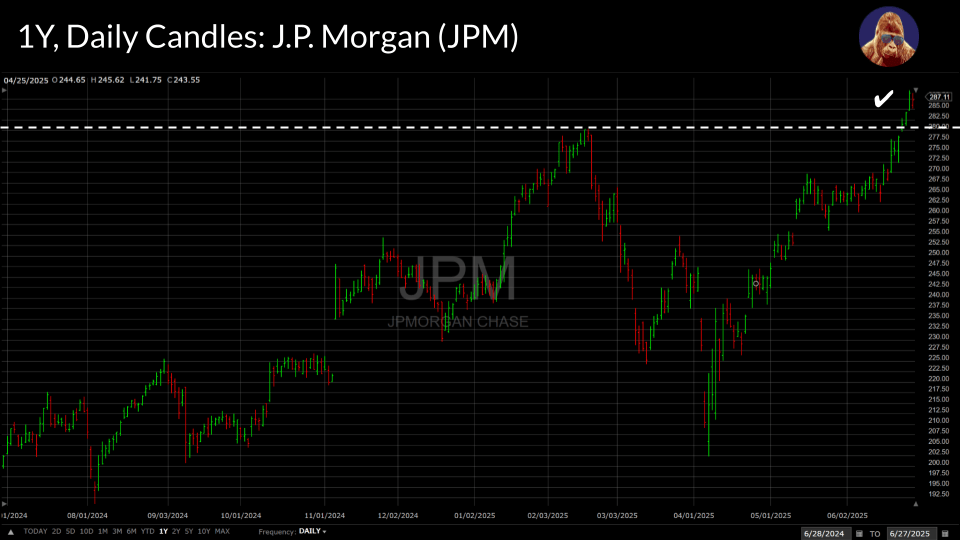

Financials (XLF) appear to have a date with the new ATH club. JPM, a 10% component of the XLF, just minted a new ATH. The outright performance of JPM could seduce buyers looking for a second-best play in the sector. Think about how many piled into AVGO after “missing” NVDA. The inflows to AVGO benefitted the SMH and all the semis in it. No reason the same can’t happen with the XLF through JPM, to the benefit of WFC, BAC, and C that all are poised for their own breakouts.

As for the financials, I am long JPM and BAC. However, these are legacy positions. I’m happy to see JPM leading the entire cohort higher. It makes sense. JPM stands head and shoulders above the rest of its cohort. I expect the XLF and its constituents — specifically BAC, WFC, and C — will follow JPM’s example and make new ATHs, lending more credibility to last Friday’s record closes.

If you’re still here and liked what you read, could you do me a favor? Consider subscribing to my website by signing up below for insights delivered directly to your inbox. If that doesn’t suit your fancy, consider dropping me a follow on LinkedIn, or sharing my work. Thank you for reading.