Weekly Performance

| S&P 500 | 2.92% |

| Equal Weight S&P 500 (RSP) | 2.52% |

| NASDAQ | 3.42% |

| DOW | 3.00% |

| Russell 2000 | 3.22% |

Talk of the Tape

Although U.S. GDP contracted for the first time since 22Q1, a robust showing from April Payrolls smoothed over immediate growth concerns.

The Week Ahead

Monday

- Palantir (PLTR)

Tuesday

- Constellation Energy (CEG)

- Arista (ANET)

Wednesday

- FOMC Meeting

- Uber (UBER)

Thursday

- Cheniere (LNG)

Friday

- Fed Speaking Tour

Macro Movers

End of an Era

This deserves priority.

During Berkshire’s quarterly event over the weekend, Buffett announced he plans to step down as CEO by year-end and recommended Greg Abel as his successor. I’ll leave the commentary on his legacy to those better equipped, but even with only a casual knowledge of markets, this feels like the end of an era.

Earlier this year, before tariffs and recession talk, Buffett built a massive cash pile for Berkshire, leaving his successors in an envious position for this downturn. He practically top-ticked his Apple sale after holding it for longer than most. He read the situation better than anyone.

What a career. Not many manage to call theirs at the top. Cheers to the Oracle.

Tariff Distortions

The preliminary reading on 25Q1 GDP came in at –0.3%, marking the first contraction in U.S. GDP since Q1 2022. An import drag of historic magnitude shaved over five percentage points off the headline number. While this was clearly a tariff distortion—the result of activity being pulled forward to front-run tariff implementation—a contraction is still a contraction. Still a bad number, just not as bad as the headline suggests.

These tariff distortions are something I believe investors should get used to. It all feels reminiscent of parsing data during COVID: stockpiling, stimulus, and supply chain shocks distorted economic signals for years. Some datasets still aren’t quite right.

The global economy is massive, and shocks take time to work through. It’s not unreasonable to expect a long duration for data distortion. Even with near-term trade resolutions, we could be dealing with it through year-end. Interpreting the data will require extra diligence. Relying on headlines alone will mislead you.

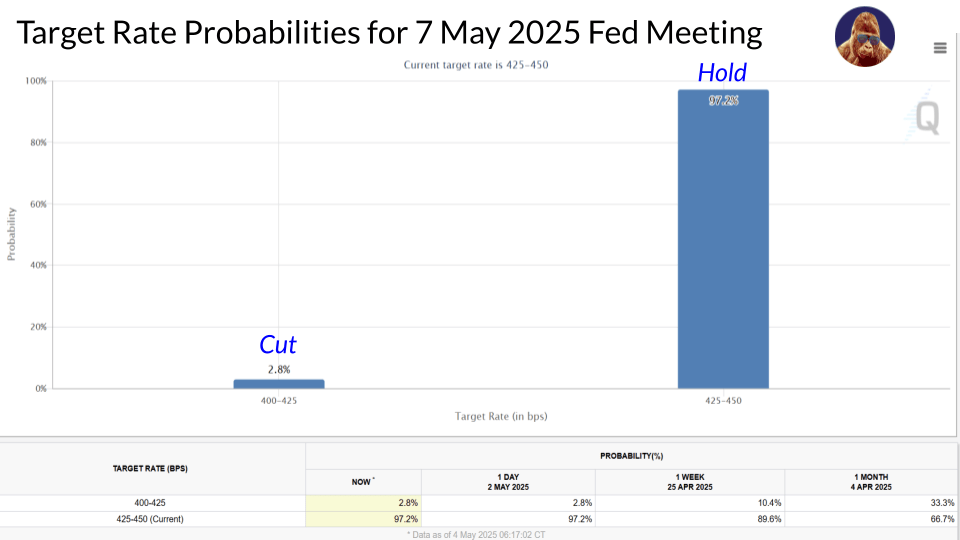

FOMC Meeting

While GDP got a lot of attention this week—rightfully so—April Payrolls mattered just as much. Without getting into the weeds, the print effectively took recession off the table for the next 30 days, along with any chance of a Fed rate cut at this meeting.

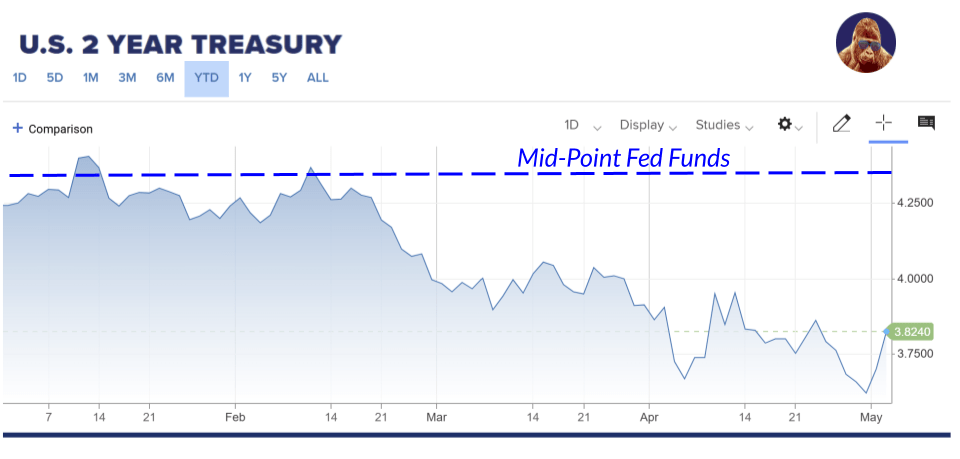

Although there hasn’t been much debate in the futures market—with CME’s FedWatch Tool steadily projecting no rate movement for some time and Payrolls reinforcing that view—the bond market disagrees. The U.S. 2-Year, often seen as the bond market’s proxy, is trading at 3.8%. That signals the economy isn’t strong enough to sustain a 4.5% Fed Funds rate. In short, the futures and bond markets are sending different messages.

In my view, Powell can’t cut after a Payrolls report like that. Right or wrong, the data suggests the Fed should lean more toward its inflation mandate than its employment mandate. It’s a tough position to be in. Not only is this data-dependent body having to parse through tariff distortions, it also has to contend (once again) with seemingly contradictory data points. Fortunately, Powell has proven adept at navigating difficult circumstances.

Fed Speaking Tour

It’s hard to know what tone the Fed will strike—or which points they’ll want to clarify—until after the FOMC. But if there’s any daylight between what they say and how markets interpret it, they’ve lined up a Wrestlemania-style media blitz on Friday to close the gap. Hearing from Fed speakers individually isn’t unusual, but to stack them all up in one day like this signals a readiness to fine-tune the message in real-time.

It makes me wonder if the Fed is actually considering cutting in accordance with the bond market and wants the airtime to soothe any volatility contradicting the futures may create. Probably not.

Here’s the lineup:

- 5:15 AM – Fed Governor Michael Barr

- 6:15 AM – New York Fed President John Williams

- 6:45 AM – Fed Governor Adriana Kugler

- 6:45 AM – Fed Governor Lisa Cook

- 8:30 AM – Richmond Fed President Tom Barkin

- 11:30 AM – Fed Governor Christopher Waller and NY Fed President John Williams

- 7:45 PM – Fed Governor Michelle Bowman, St. Louis Fed President Alberto Musalem, and Cleveland Fed President Beth Hammack

Micro Movers

Range Bound… Until We’re Not

Markets believe we’ve seen peak tariffs, and there’s now incremental clarity on the subject. I think that sets the stage for the S&P 500 to trade within a range—at least until greater clarity arrives. To understand how we got here, a quick timeline of April:

- Investors saw Liberation Day and were like… okay, peace. Mass exodus. Market falls.

- The White House puts up a front, claiming the U.S. isn’t interested in negotiating. That stance lasted until we nearly had a credit event in the Treasury market.

- Trump shifts tariffs from country-specific Liberation Day rates to a universal 10%.

- From that point on, the news flow turns positive. The White House now seems eager to hand out trade deals like Oprah with Pontiacs in 2004. Both China and the U.S. stated publicly that the current tariff situation is unsustainable.

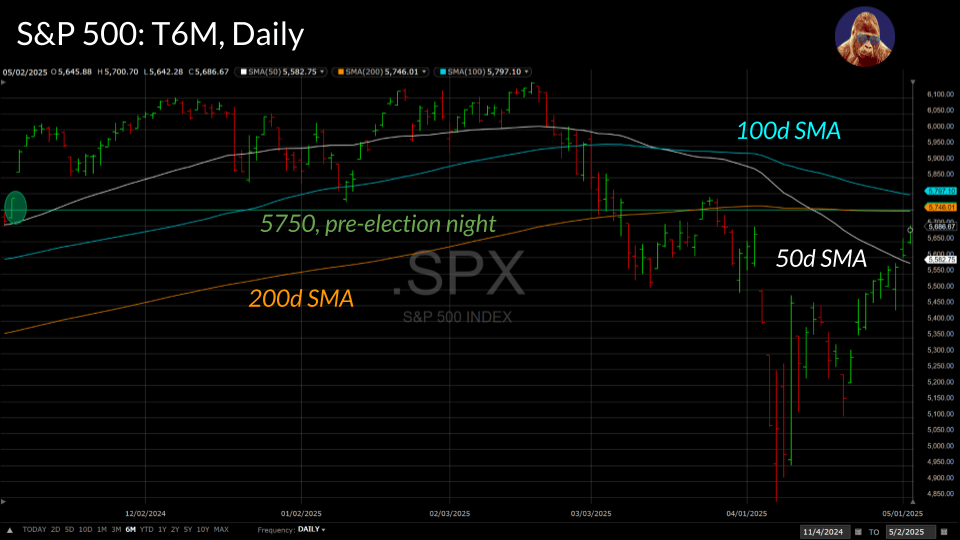

By the end of April, markets feel we’ve seen peak tariffs—setting the lower bound near 4800—and a tariff floor, which implies an upper bound. I think the S&P 500 is still trying to find that ceiling. The 200-day SMA is within striking distance. Perhaps resistance lies there. Maybe it’s a little higher, around 5750, where the S&P 500 closed the night of Trump’s election victory (not the gap up that followed).

If we were to break above these upside checkpoints, I wouldn’t be a buyer. Given what I view as the risk to earnings and the likely outcome of tariff policy, I feel this is a bear market rally. I am not sure when the market turns, what causes it, or if it means we need to retest the lows. I just don’t see the trade saga ending here and stock returning to the highs so easily.

Upside Risks

First and most obvious: trade deals. For the last two weeks, the Trump administration has been hinting at a deal with an unnamed country. The consensus is that it’s either India or Japan. Given the high-profile nature of such a deal, I imagine the market has already priced it in. That said, Payrolls left me feeling tactically bullish. The resilience gives speculators permission to buy dips. If a deal emerges—especially one with terms that appear replicable—it could serve as a genuine buy-the-news catalyst.

Exemptions are another potential upside trigger. Both China and the U.S. have quietly been exempting tariffs on goods they would really rather not go without. We’ve seen carve-outs on semiconductors, computers, and more. At a certain point, the market may begin to ask: “What are the tariffs actually on?” If they don’t cover the companies driving the majority of S&P 500 earnings, maybe estimates don’t need to come down.

Downside Risks

The effective trade embargo between the U.S. and China is unlikely to avoid causing some degree of slowdown or even a shallow recession. In my view, the downside scenario comes down to a matter of timing. Timing the market is a fool’s errand. As such, this is something I keep in mind but out of actual allocation decisions.

Right now, I believe the market is pricing in a scenario where Q2 results are weak, but Q3 guidance implies Q2 was the trough. If that’s the case, 4800 may very well have been the bottom, and we won’t need to retest it. But if markets start to believe that the trough in earnings won’t arrive until Q3 or Q4, a retest or new lows becomes far more likely.

Earnings Highlights

- Palantir (PLTR): The definition of AI-ROI. Bulls have regained control, and I still see it as the future of government contracting. I’ll be curious for any insight they may have on DOGE’s priorities on the defense budget.

- Constellation Energy (CEG) & Arista Networks (ANET): Both names were crushed in the AI-wreck, but look like they want to rally. If they break out, it could revive the AI trade and reenergize risk-on positioning.

- Uber (UBER): One of my favorite setups—bulls are clearly back in charge. The business proved resilient during 2022. Perhaps this quarter reminds the market of that, allowing the stock to break resistance in the low-to-mid 80’s.

- Cheniere Energy (LNG): There’s chatter of a new U.S. natural gas export deal, possibly tied to an executive order facilitating LNG trade. If management can confirm the company is a beneficiary of these developments, the chart is prime to move higher.

I am long PLTR, UBER, and LNG.