Weekly Performance

| S&P 500 | -4.25% |

| Equal Weight S&P 500 (RSP) | -2.64% |

| NASDAQ | -5.77% |

| DOW | -2.93% |

| Russell 2000 (VTWO) | -5.69% |

Talk of the Tape

Although many attribute the prior week’s decline to a more balanced economic debate pressuring multiples, I believe the pullback is more about timing: the data being used as cover to sell ahead of what has been a historically weak seasonal period for stocks, particularly so over the last two years.

The Week Ahead

Monday

- Oracle (ORCL)

Tuesday

- n/a

Wednesday

- CPI

Thursday

- Initial Jobless Claims

- PPI

- Adobe (ADBE)

Friday

- n/a

Macro Movers

September’s fire sale feels a fitting way to signal the end of summer’s seasonal strength to make way for the weakness synonymous with late-September and October.

As I noted earlier, I don’t buy that data drastically changed anyone’s view of the economy. While most data continued to surprise to the downside, there are still pockets of strength where you’d expect them (services). In my view, this data reflects more of the same: a Goldilocks scenario, consistent with the illusive soft-landing.

That said, it’s worth pointing out that the small contingent on Wall Street arguing for the Fed to skip a September cut has disbanded. Recent downward revisions have weakened data points that initially appeared more resilient.

In summary, the data aligns with Powell’s message from Jackson Hole: as inflation falls and the job market moderates, interest rates have become too restrictive and need tuning. I don’t expect upcoming CPI, PPI, or jobless claims to change that. Ideally, we see CPI and PPI slightly below expectations, and jobless claims reassure us that labor market cooling isn’t turning into something more concerning. My real worry would be if CPI and PPI are too low, signaling a potential recessionary shift in consumer and producer behavior.

Forecasts:

- CPI: Core YoY 3.2%, Core MoM 0.2%

- PPI: Core MoM 0.2%

- Jobless Claims: 225k

Micro Movers

With Nvidia officially in the rearview, earnings season is effectively over. However, two notable companies tied to the AI-narrative, Oracle (ORCL) and Adobe (ADBE), report this week.

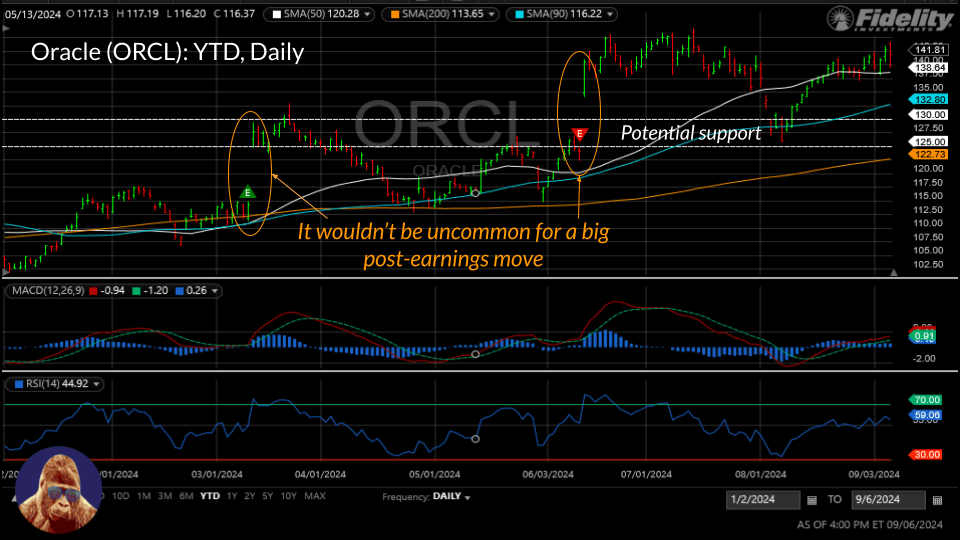

Oracle (ORCL): Expectations are high for this top-five U.S. hyperscaler as it heads into its earnings call within 5% of its all-time high. While I don’t own the stock, I expect a strong quarter. However, since Nvidia’s report, the market has adopted a “sell first, ask questions later” approach to tech, meaning the stock may not be rewarded for solid performance. I’d consider trimming or selling covered calls ahead of the report because I feel the odds are skewed toward the quarter creating a buying opportunity Tuesday morning.

Adobe (ADBE): Long-time readers will remember my misadventure in this name. After selling it at a loss, I haven’t followed Adobe closely. However, the company is back on my radar as concerns over the return on AI investment are partly responsible for tech’s weakness. My original thesis was that Adobe was well-positioned to prove AI’s ROI, and perhaps this quarter will help ease those concerns.

Leave a Reply