Retired November 2025 – 9:25

Start the week with the “9:25” – you’ll get up to speed on what’s moving your money in the markets by the 9:30 open. Formerly, The Market Brief.

-

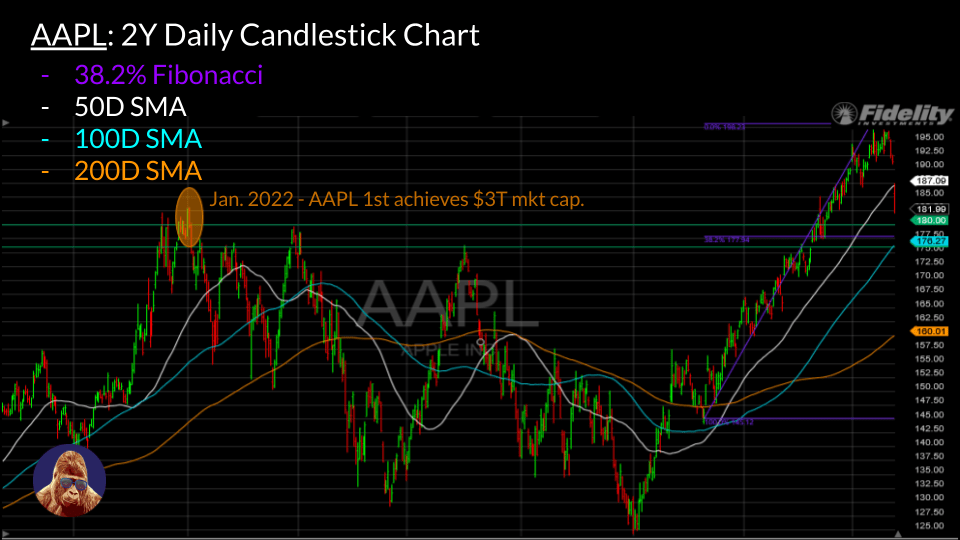

The Week Behind Despite July Payrolls relaxing interest rates, stocks faded halfway through Friday’s session. While there is no clear consensus on the downside catalyst, I suspect the 5% post-earnings decline in Apple shares played a role. As a result, all major indices ended the week lower: the Dow down 1.11%, the S&P 500 down…

-

The Week Behind While GDP stoked the inflationary fires on Thursday, Friday’s PCE dampened inflationary embers, allowing the majors to tally winning weeks on the backs of strong corporate results. The Dow finished the week ~0.6% higher; the S&P 500 added ~1%; and the NASDAQ gained ~2%. Highlights Monitoring the Macro Despite abundant micro data…

-

The Week Behind With the Fed blackout window in effect and economic data failing to sway expectations of a 25 bps increase, corporate earnings drove index performance this week. The Dow outperformed, gaining approximately 2%, bolstered by solid quarters from big banks, regionals, and healthcare. The NASDAQ underperformed, experiencing a 0.60% drop, as Netflix and…

-

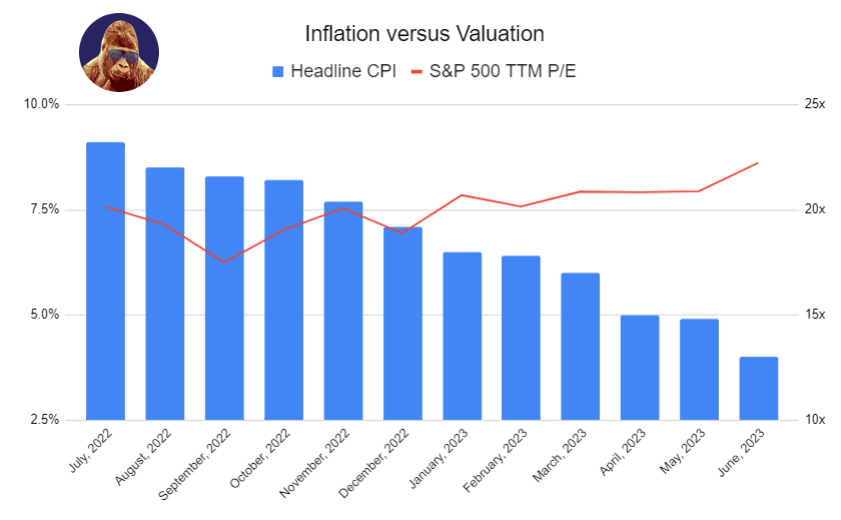

The Week Behind It was a good week for stocks as CPI showed that inflation moderated more than anticipated in June. The soft number extended the downward reversal in yields and the dollar that started with June Payrolls. Lower rates and a weaker dollar created additional runway for stocks to run. For the week, the…

-

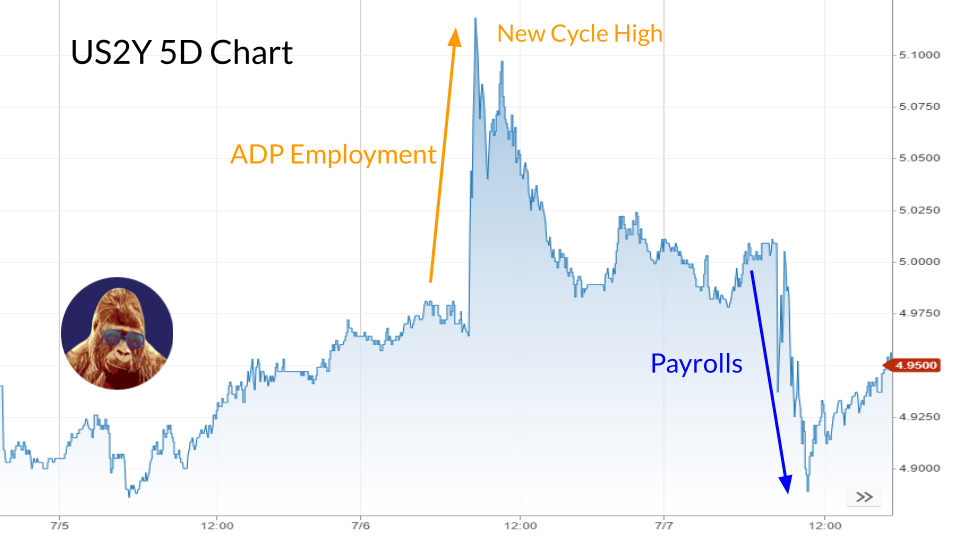

The Week Behind Despite Payrolls painting a more balanced inflationary picture, concerns about tighter monetary policy, fueled by hawkish FOMC Minutes and a remarkably strong ADP employment number, pushed yields to uncomfortably high levels. This upward move in yields put downward pressure on stocks, resulting in a ~1% decline for the S&P 500 and NASDAQ.…

-

The Week Behind The momentum in stocks continued as the ECB forum on central banking and PCE report failed to challenge the bull case surrounding monetary policy and recession. As a result, the major indices finished the week about ~2% higher, marking a small triumph for the catch-up thesis. Highlights Early Earnings Informants Last week,…

-

The Week Behind This week, the major indices experienced a ~1.5% decline as Jerome Powell testified to Congress at the Biannual Report on Monetary Policy. While some attribute the action to headlines from the event, I hold a different perspective. Powell’s testimony was consistent with the June FOMC Meeting; therefore, no new information was presented…

-

The Week Behind The rally forged on as the Fed delivered the highly anticipated hawkish pause, and corporate earnings verified more AI-winners. These developments contributed to the market’s momentum and added fuel to the fear of missing out (FOMO) sentiment. Although Friday’s session was turbulent, all major indices ended the week with gains. The NASDAQ…

-

The Week Behind The performance of the major indices reflected an inconsequential week devoid of influential earnings or economic releases. Although the S&P 500 registered a new bull market close, marking a 20% increase from the October low, it only recorded a modest gain of 0.39% for the week. The Dow advanced by 0.34%. The…

-

The Week Behind Benign labor data, solid corporate earnings, a surprisingly clean debt ceiling resolution, and dovish Fed reporting created a “goldilocks” feeling in the stock market. Notably, the rally’s breadth expanded beyond the technology sector, encompassing other parts of the market that have struggled in the past three months. This broadening was reflected by…