Before we get started, I hope you all had a lovely Easter holiday and are feeling rested as we get back to work.

Was last week nothing more than a short squeeze?

It looks like it.

There has been no change in the sentiment surrounding the war. Going into the weekend, the situation with oil got worse, not better. The best-performing basket of stocks? Goldman’s Most Shorted Index put in a one-day 7.1% rally: the second-biggest in a little under a year.

That said, every durable bottom starts with short covering.

The next logical question: Is this a bull trap/bear market rally, or is this the real deal?

It is impossible to know, but my point is that the fact that all we’ve seen so far is a short squeeze doesn’t tip the scales in the debate of whether or not we’ve seen “the bottom” or just “a bottom.”

So… now what?

Well… we’ve witnessed the short squeeze; the “easy money” has been made. There is now a higher bar for incremental upside at the same time shorts are undoubtedly looking for their next entry. The tactical argument to buy stocks because “stocks were oversold” no longer holds water.

In the immediate term, the playing field is balanced.

Therefore, we play the confirmation game.

Confirmation can come from a number of sources: the more, the better. The tradeoff is the initial upside that comes with buying while the market remains in flux for the assurance that the money you put to work at 4:00 PM isn’t going to be down 5% at 9:30 AM the next day.

Here is a potential set of criteria for confirmation that the worst is behind us:

- The VIX or oil collapses.

- The S&P 500 convincingly regains the 200d SMA.

- Equities in the oil (CVX, XOM, FANG, OXY, etc.) and fertilizer (CF) spaces collapse.

I italicized “convincingly” and “collapses” for a reason. I wish I could be more articulate, but this is a “feel” thing for me. While there are technical levels to watch, I use those two words sparingly because, to me, they imply an absence of ambiguity. You should be able to look at the chart of the VIX, oil, CVX, CF, etc., and say, “Yeah, the top is in.” You should be able to look at the S&P 500 and say, “Yeah, the 200-day is our friend again.”

Key

Macro Economic Events

Corporate Earnings

High Importance

See Note Section Below For Additional Insight

Monday

ISM Services | Est: 55.4%; Prior: 56.1% | 1000

Tuesday

Chicago Fed President Austan Goolsbee | 1235

Fed Vice Chair Philip Jefferson | 1750

Wednesday

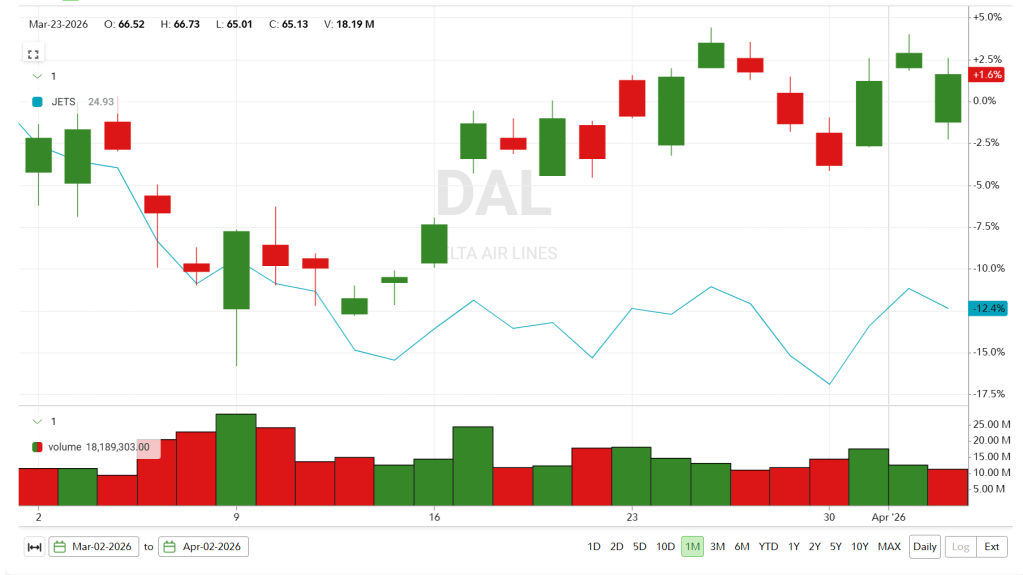

Delta Airlines | BTO

Talk about relative strength. Despite the neighborhood (JETs ETF) being in a bona fide correction — down ~12.5% since the war began — Delta is showcasing relative strength. This knowledge isn’t an advantage; the source of the outperformance is clear: Delta owns a refinery. This hedge is clearly paying off for shareholders.

Across the industry, companies are reporting their best month in years as travelers look to book their trips before jet fuel surcharges price them out of a potential vacation. I’m interested to see how the market reacts when the industry’s best-in-breed reports. Is a positive result sold on the notion that the rest of the year’s demand just got pulled forward into the quarter? We’ll find out. But, if it responds well post-report, I will consider taking a flight in the stock.

San Francisco President Mary Daly | 1305

Minutes of Fed’s May FOMC meeting | 1400

Thursday

February’s Personal Consumption Expenditures

Personal income | Est: 0.3%; Prior: 0.4% | 0830

Personal spending | Est: 0.5%; Prior: 0.4% | 0830

PCE index | Est: 0.4%; Prior: 0.3% | 0830

PCE (year-over-year) | Est: 2.8%; Prior: 2.8% | 0830

Core PCE index | Est: 0.4%; Prior: 0.4% | 0830

Core PCE (year-over-year) | Est: 3.0%; Prior: 3.1% | 0830

GDP (second revision) | Est: 0.7%; Prior: 0.7% | 0830

Initial jobless claims | Est: 210,000; Prior: 202,000 | 0830

Wholesale inventories | Est: -0.5%; Prior: -0.5% | 1000

Friday

March’s Consumer Price Index

Consumer price index | Est: 1.0%; Prior: 0.3% | 0830

CPI year over year | Est: 3.3%; Prior: 2.4% | 0830

Core CPI | Est: 0.3%; Prior: 0.2% | 0830

Core CPI year over year | Est: 2.7%; Prior: 2.5% | 0830