Key

Macro Economic Events

Corporate Earnings

High Importance

See Note Section Below For Additional Insight

Monday

Fed Chair Jerome Powell speaks at Harvard | 1030

Tuesday

Job openings (Feb.) | 7.0 million est; 6.9 million prior | 1000

Chicago Fed President Austan Goolsbee | 1200

Fed Governor Michael Barr | 1500

Fed Vice Chair for Supervision Michelle Bowman | 1710

McCormick (MKC) | BTO

Wednesday

LambWeston (LW) | BTO

Conagra (CAG) | BTO

ADP Employment (March) | 42,000 est; 63,000 prior | 0830

St. Louis Fed President Alberto Musalem speaks | 0905

Fed Governor Michael Barr speaks | 0910

S&P final U.S. Manufacturing PMI (March) | 52.4 est; 51.6 prior | 0945

ISM Manufacturing (March) | 52.0% est; 52.4% prior | 1000

Thursday

Initial jobless claims (March 28) | 210,000 est; 210,000 prior | 0830

Friday

GOOD FRIDAY: Stock Market is Closed; Bond Market is Open.

U.S. employment report (March) | 45,000 est; -92,000 prior | 0830

U.S. unemployment rate (March) | 4.5% est; 4.4% prior | 0830

U.S. hourly wages (March) | 0.3% est; 0.4% prior | 0830

Hourly wages year over year (March) | N/A; 3.8% prior | 0830

S&P final U.S. services PMI (March) | 51.1 est; 51.7 prior | 0945

Gorilla Takes

The literal fog of war renders it impossible to forecast what will be important and what will fall by the wayside. It’s a headline-driven market. However, I will be listening to what MKC, LW, and CAG have to say about consumer tendencies. These companies all benefit when households opt to eat more meals at home than out. It’s a better read on sentiment than a survey.

Otherwise, one thing to be aware of is that Good Friday aligns with the government payrolls survey for March and is a market holiday for equities. The schedule landed this way a few years back. Nothing to be afraid of. In fact, allowing markets the weekend to digest – given the current volatile backdrop – is probably a good thing.

Before letting you go, I want to focus your attention to a few matters that should continue to matter beyond the week: software has a new enemy, only the general remains, the question all investors should have in their minds.

Shall we?

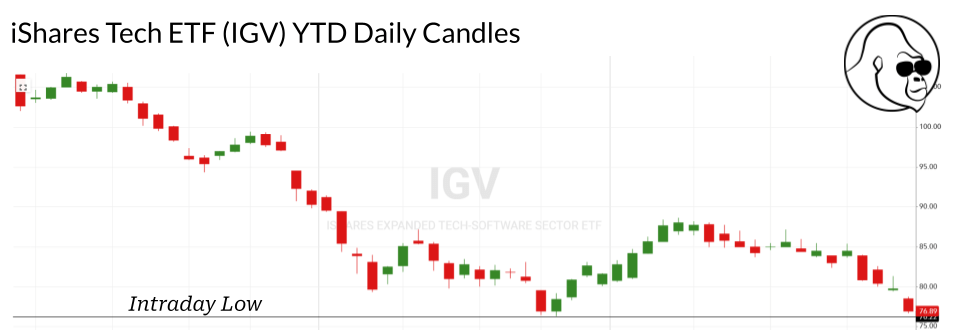

Return of an Old Enemy

In a recent video, I hypothesized that the bounce in software was a trap. Although IGV didn’t make a new intraday low, it did make a new closing low… Either way, I’d say this is confirmation that the recovery that started February 23rd was a bull trap.

Surprisingly, it happened without a change in the wartime environment that created the conditions for a recovery in the sector: higher energy costs dilute the margins of many companies, but not software. If you are looking for insulation from energy-related headwinds, then software makes a lot of sense.

Over the past 12–18 months, we lived in a tame yield environment and, perhaps, have forgotten how detrimental an uncontrolled rise in yields can be to asset-light software stocks: higher yields reduce the present value of their future earnings (DCF math).

The upward pressure from yields is the only new variable for this wartime backdrop; thus, I believe it to be the most likely culprit for software’s failure to act as a safe haven as it did when this war first started. Although I believe it is only a matter of time before yields come down, what happens before then is impossible to handicap.

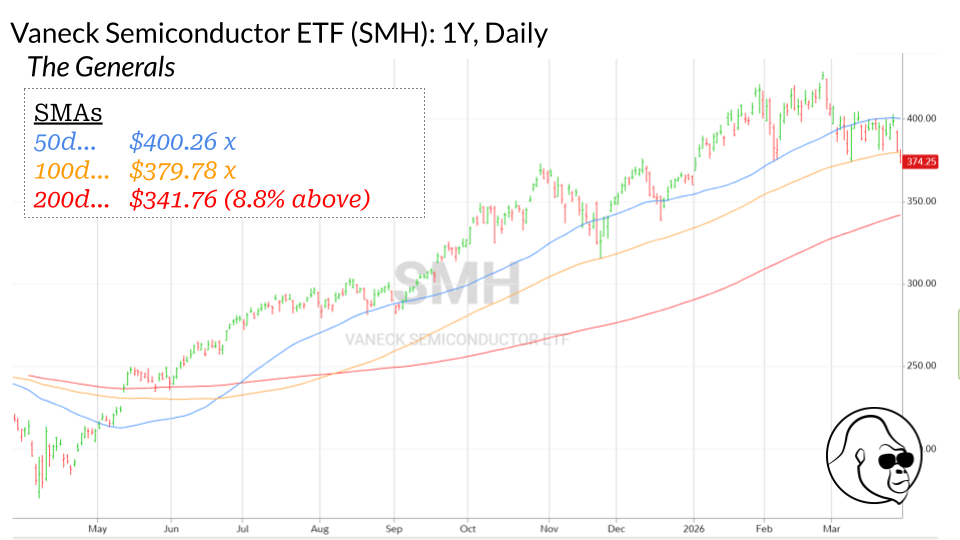

12% of the S&P 500 is in Danger

Make no mistake, the semiconductors have been the leadership group since November 30, 2022 when OpenAI unveiled ChatGPT, capturing the public’s imagination and capital.

The index is hanging on to 100d SMA for dear life. Nvidia is on the ropes. If these generals — which make 12% of the market cap — fill the ~9% gap to the 200d (seems like a formality at this point), we’ll surpass the 10% correction threshold swiftly on the S&P 500. Many of those who have remained constructive likely fold. However, there is a silver lining:

“They come for generals last”

When market leadership finally falls, another box gets checked for nearing the end of a downside move: positioning gets wiped out, sentiment resets, and there is nothing more to sell.

Month to date, there is nothing left to go after. Sure, year-to-date there is a little green that can go red, but bears are clearly running out of easy targets to maul.

Don’t Panic; Plan.

What should you be buying once this is over?

That is the question. Because, this will end. And, when it does. Stocks won’t wait.

Those who know what to do when the time comes will do better than those who don’t. Ultimately, your answer depends on your circumstance, but I’ll share two places I’m constructive in the long-term post-war.

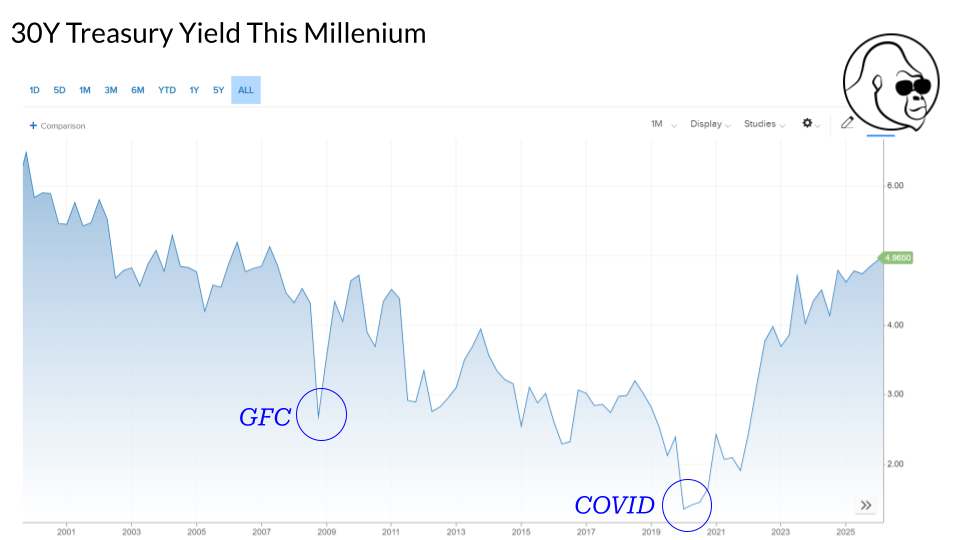

Financials make sense. Oil between $90-$110 didn’t kill demand in the 2010s. Our economy has never been less levered to oil. It won’t kill demand this time. That means the post-war economy — holding all else equal — will still support the loan-making activity that makes the financials extremely attractive.

Otherwise, traditional defense seems obvious. Although these stocks have too forgotten how to go up, they haven’t forgotten how to make munitions, which will need to be restocked.

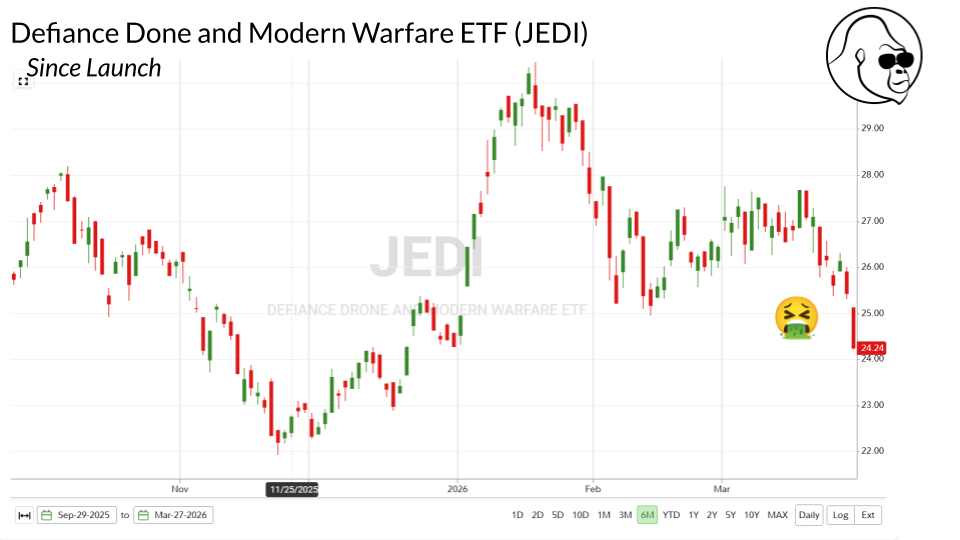

The demand will be there. Execution on supply will determine how well any individual name does. But, instead of choosing one, especially in the very new world of drones, I have opted for the ETF route.

I am long the JEDI ETF, which holds a nice basket of the future-of-warfare names. Although it projectile-vomited on Friday, I’m accumulating this one slowly. The ITA scratches a similar itch and is probably higher on quality metrics.