Key

Macro Economic Events

Corporate Earnings

High Importance

See Note Section Below For Additional Insight

Monday

Construction Spending (Jan.) | 0.1% est; 0.3% prior | 1000

Tuesday

U.S. productivity (Revision, Q4) | 1.8% est; 2.8% prior | 0830

S&P flash U.S. services PMI (March) | No Forecast Available; 51.7 prior | 0945

S&P flash U.S. manufacturing PMI (March) | No Forecast Available; 51.6 prior | 0945

Wednesday

Cintas (CTAS) | BTO

Paychex (PAYX) | BTO

Thursday

Initial Jobless Claims (March 21) | 210k est; 205k prior | 0830

Fed Speakers

Fed Governor Lisa Cook 1600

Fed Governor Stephen Miran 1830

Fed Vice Chair Philip Jefferson 1900

Fed Governor Michael Barr 1910

Friday

Consumer Sentiment (Final, March) | 54.0 est; 55.5 prior | 1000

Gorilla Takes

I have a few. To be fair, all are taken from what I said on Charts and Checks EP36… but, admittedly, I didn’t do a great job explaining them in real-time.

Let’s recap my take on PPI, refresh your memory as to why CTAS and PAYX matter, and wrap up with a tactical position I see with asymmetric upside…

Can’t wait to see how that one works against me. What’s the saying?

“Markets work in the way that renders the most people foolish”?

Yeah. That would be the one.

Rate Hikes… Really?

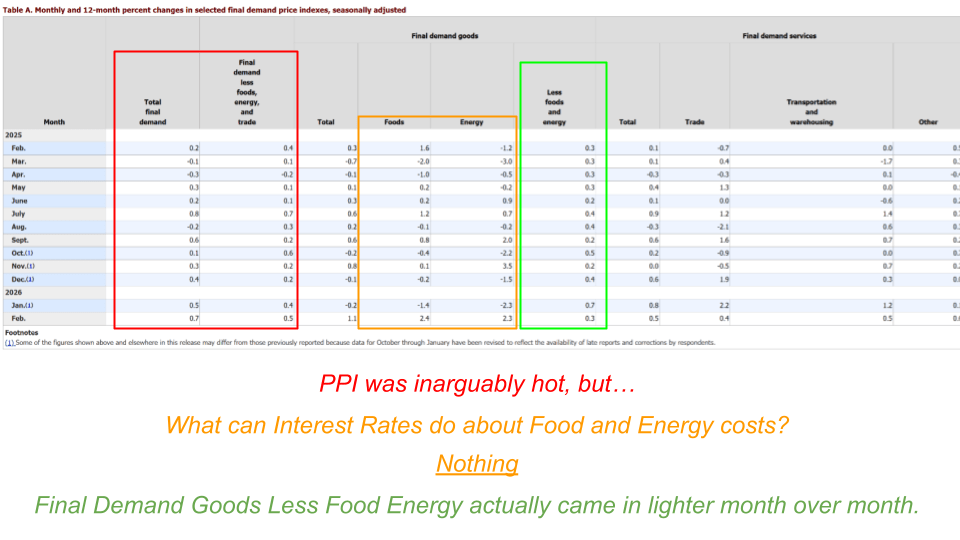

PPI inflation, which has often served as an offset for bulls when other measures get too hot, offered no such refuge.

Not here to argue it wasn’t. I am here to make the case that rate hikes won’t make a difference. Food and energy costs were the outsized contributors to this hot number.

Increasing Fed Funds will not lower anyone’s energy or food bill.

The flare up in food remains a mystery to me. This February number shouldn’t include any potential impact from the surge in fertilizer prices associated with the supply disruption since the de facto closure of the Strait of Hormuz.

What is 0.25-0.50% on Fed Funds going to do to ease this disruption? Nothing.

Energy is a little less opaque. The most likely explanation is energy demands from AI-factories/data-centers. I believe a policy intervention – or an industry-solution – will need to be the fix here.

What is a 0.25-0.50% increase in Fed Funds going to do to AI demand?

Anything? I don’t think so.

For what it’s worth, policymakers are reportedly already discussing measures to ensure that the hyperscalers – those responsible for the disproportionate surge in demand – bear the cost of that increase, thus preventing the imposition of an excessive financial burden on ordinary citizens.

All of that to say this:

Those on the FOMC know the interest rate tool won’t have the desired effect on these categories.

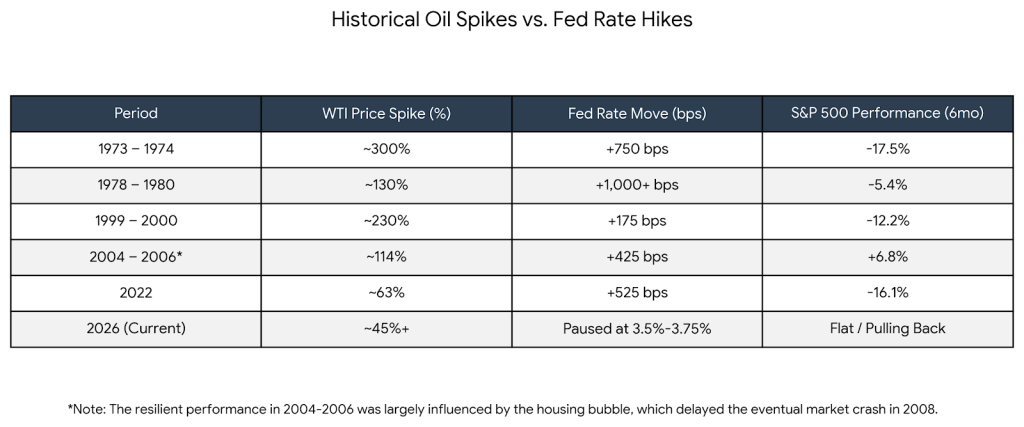

Raising interest rates would only make it harder for those already struggling the most by increasing their credit rates at the same time it becomes more expensive to buy food and groceries… And, finally, hiking rates into an energy shock has never once ended well for anyone.

I am not oblivious to the hawkish rhetoric but don’t yet believe it. I believe the Fed is jawboning the market, which has been an effective tool over the last half decade. I don’t blame them for falling back on it.

Cintas and Paychex

The strength of their business — supplying consumables and volume-related services — is entirely dependent on the strength of the small- and medium-sized businesses they serve in the U.S.

Personally, I was shocked by FedEx’s guidance. It appears as though the increased price of fuel has yet to slow down economic activity, which bodes well for CTAS and PAYX. I neither trade nor invest in these names, but always view the quality of their report (not the next-day price reaction) as tea leaves for an integral part of the U.S. earnings picture.

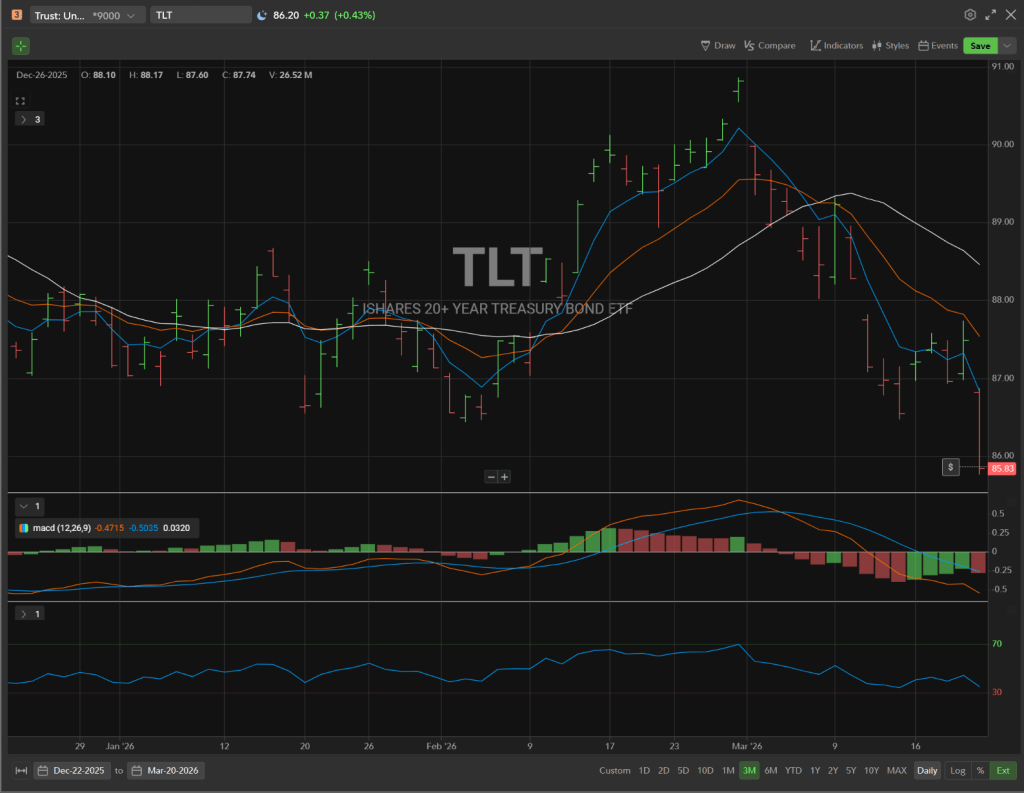

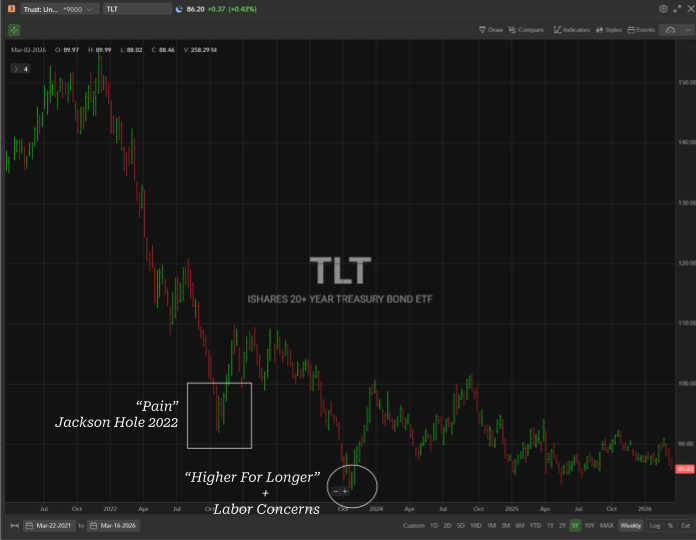

I Can’t Believe I Am Buying Bonds

Quick lessons on fixed income: the yields and face value (price) are inversely correlated. If yields move higher, prices move lower. If yields move lower, prices move higher.

So, when buying bonds tactically, what is the thesis? It is that yields will go lower.

I see two scenarios:

- Conflict in Iran gets worse or remains bad. Oil goes higher or remains between $100-$120. Eventually, instead of pricing-in inflation by going higher, yields will move lower to price-in an energy-shock recession as investors ditch equities for fixed income in a textbook “flight to safety.”

- Conflict in Iran ends. Oil moves lower. Yields move lower as overly hawkish expectations surrounding inflation get priced-out.

I don’t see a third outcome; and, in either of the binary outcomes, yields on the long bond (10-30 year duration) would be hard-pressed to sustain these levels.

Straight up on price –> Straight down on Yields

You can play this through the TLT (iShares 20+ Year Treasury Bond ETF). I’ve started with half of a position after Friday’s horrific close. I didn’t go “all-in” because I could imagine a scenario in which there is one more flush and the bond markets look like they did in October 2023. However, I could also imagine a scenario where there is a swift conclusion and markets are forced to unwind a meaningful amount of the hawkish tension in prices.

Reaching levels that require another catalyst for meaningful downside follow through.