Key

Macro Economic Events

Corporate Earnings

High Importance

See Note Section Below For Additional Insight

Monday

S&P Manufacturing PMI (Final, February) | 51.2% est. & 51.2% prior | 0945

ISM Manufacturing PMI (February) | 51.7 est. & 52.6 prior | 1000

Tuesday

CrowdStrike (CRWD) | ATC

Wednesday

ADP Employment | 49k est. & 22k prior | 0815

Broadcom (AVGO) | ATC

Veeva Systems (VEEV) | ATC

Thursday

Initial Jobless Claims | 215k est. & 212k prior | 0830

Marvell (MRVL) | ATC

Costco (COST) | ATC

Friday

February Nonfarm Payrolls | 0830

- Job Creation… 54k est. & 130k prior

- Unemployment Rate… 4.3% est. & 4.4% prior

- YoY Hourly Wages… 3.7% est. & 3.7% prior

- MoM Hourly Wages… 0.3% est. & 0.4% prior

Gorilla Takes

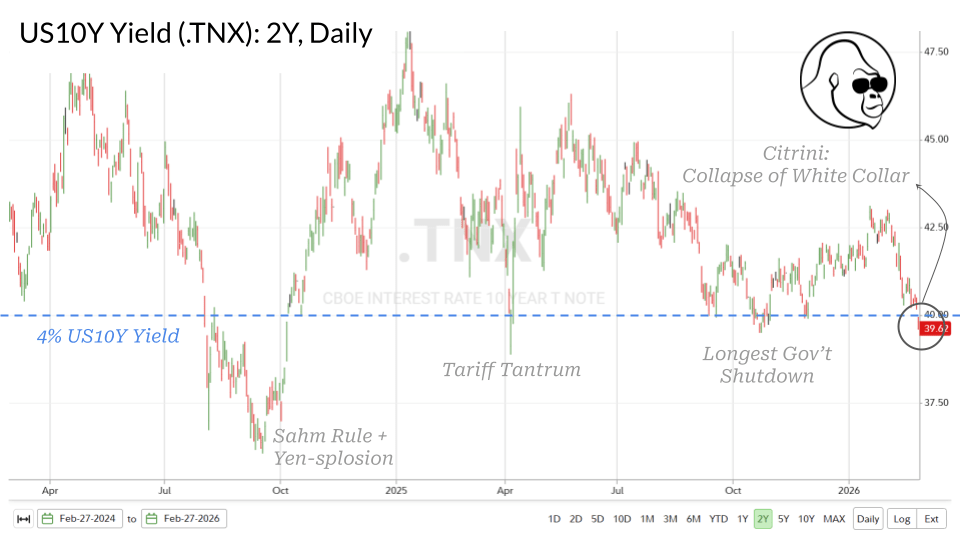

PMIs

A lot of different parts of the market can work (will get re-rated) with lending costs and competition for capital when the benchmark US10Y yields are this low… it will be interesting to see if strong PMIs can bring the benchmark yield back above 4%.

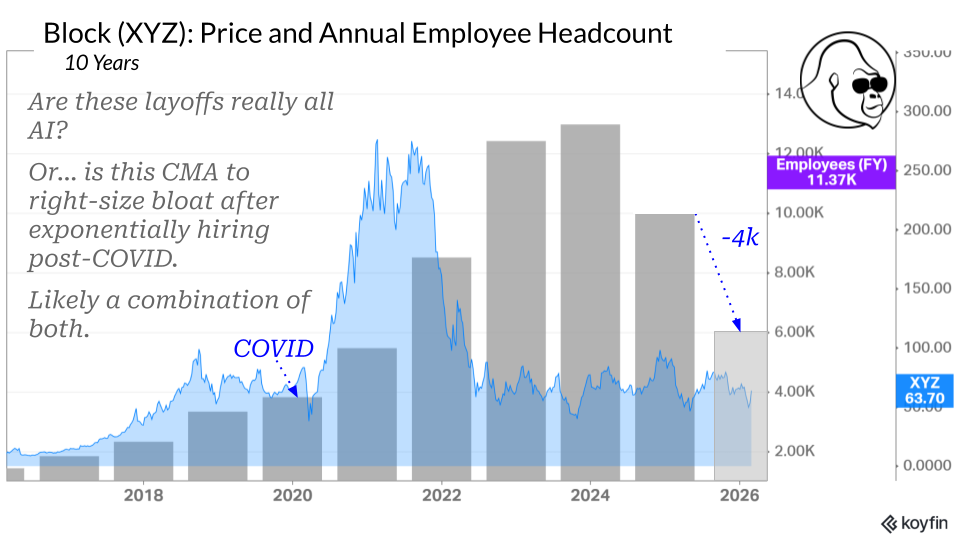

Many might be curious as to why PPI didn’t cause a spike in yields. I believe that is because of Jack Dorsey’s decision to let go of 40% of their workforce, attributing the decision to AI efficiency.

I harbor skepticism. Jack Dorsey ran Twitter into the ground and definitely reads his press clippings. He doesn’t want to be the villain. I think he is using AI as cover to right-size his bloated business. But, that doesn’t matter…

Through the fear-tainted lens of today’s market, no one is asking how much of this about AI and how much of this is about bloat. The herd is rushing to the conclusion that it is all AI, reinforcing Citrini’s thesis on the collapse of the white-collar workforce, which is really bad for earnings.

Significant unemployment – especially if concentrated in higher earners – will cause a spending collapse (a major S&P 500 earnings risk), making inflation the least of our worries. This risk spurred a flight to safety, shown by falling yields and the outperformance of recession-proof sectors (Healthcare, Utilities, Telecom) while cyclical sectors (Financials, Discretionary, Software) saw major losses.

CrowdStrike (CRWD), Veeva (VEEV)

No change in my thoughts on CRWD. While Claude’s vulnerability scanner is impressive, it is iterative in nature as opposed to transformative. In other words, it is not new nor eliminates the need for a full-suite cybersecurity provider. As such, I expect an awesome quarter, unencumbered by M&A costs vis-à-vis PANW.

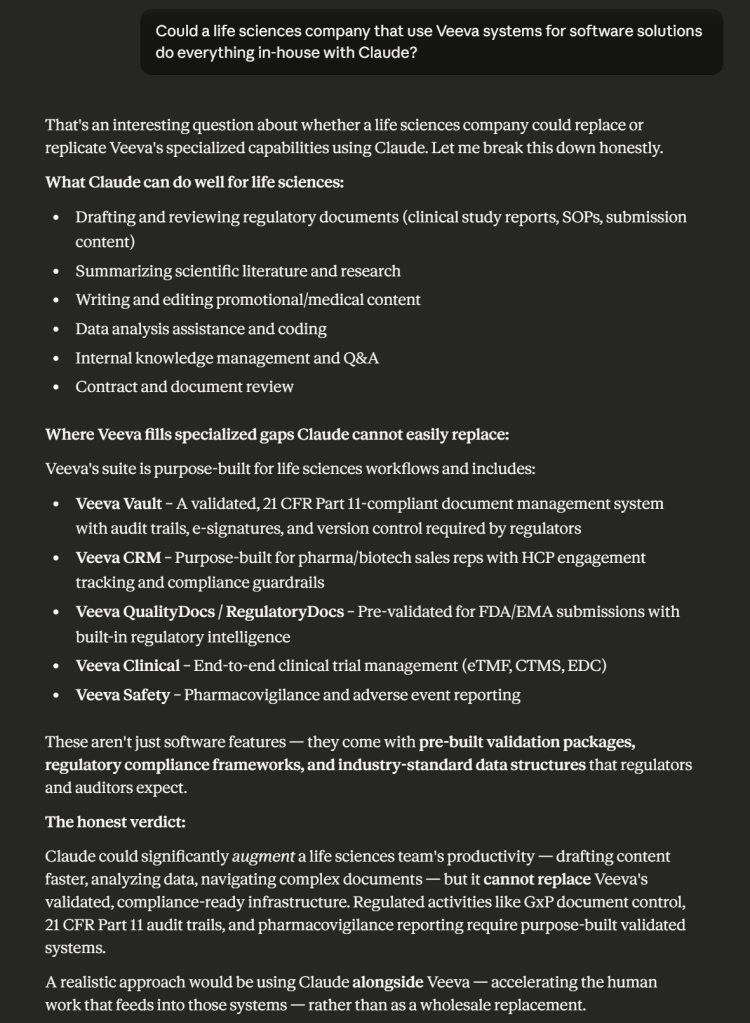

Veeva is a software company for life science companies. Due to its industry, an important part of the value proposition is HIPAA compliance. Although I respect the impressive capabilities of AI, I maintain my overall thesis that the limitations mean Claude is not quite ready to replace software in an instant.

Disagree? Okay, but you’ll find that Claude itself agrees with me.

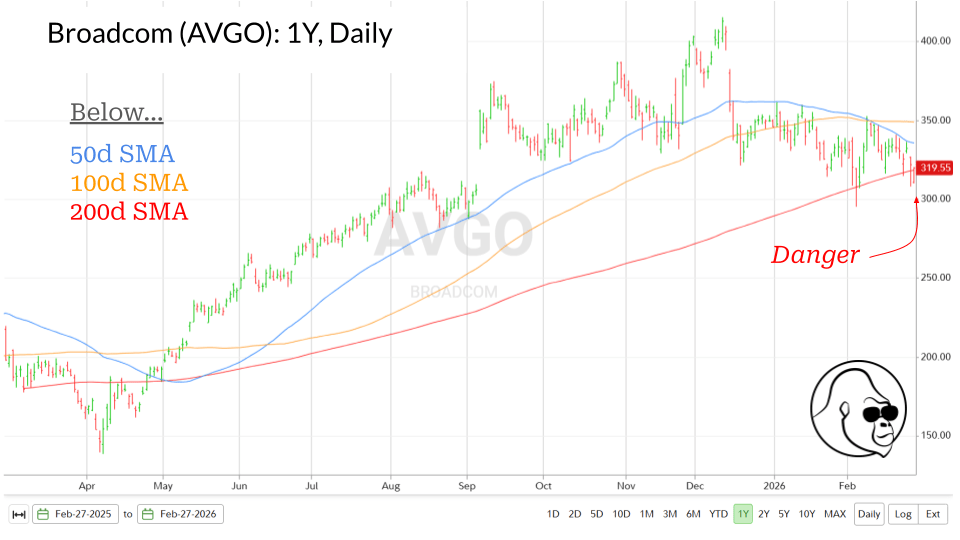

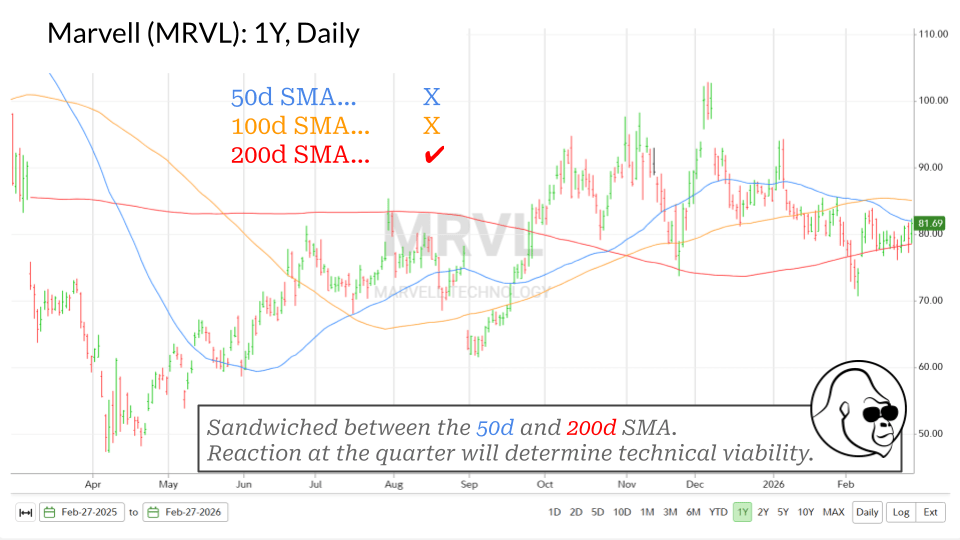

Broadcom (AVGO), Marvell (MRVL)

AVGO appears to be falling apart ahead of their quarter.

I attribute the acute weakness to AVGO’s software business. Once considered the perfect complement to their hardware business, ~50% of revenue coming from software is now considered a sin.

MRVL seems a little sturdier by comparison, but NVDA delivered the bag of all bags only to be rewarded by shedding 10% in the two sessions that followed. If you approach, do so with caution. Personally, I think there are better areas of the market to search for opportunities.

That said, up to this point, the bear market in technology – particularly in software – is completely sentiment-based. If this negativity isn’t verified by the fundamentals, the door is open for V-shaped recoveries. Of course, timing these moves is impossible, and the pain associated with holding is real. That said, periods of de-risking and de-leveraging ultimately set the stage for a lucrative, enduring bull market.

If you are an investor, let this play out; have a plan; stick to it.

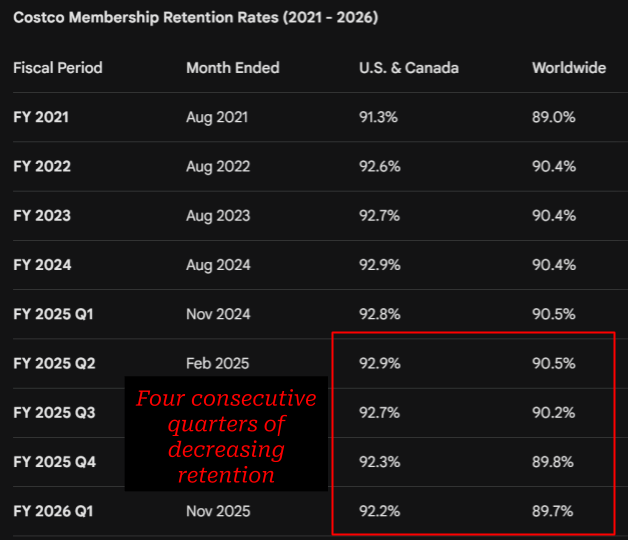

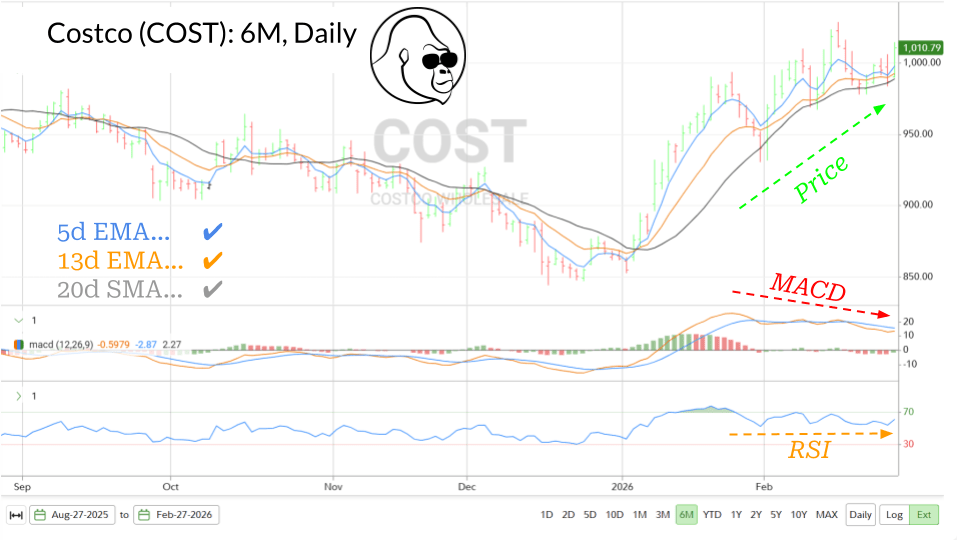

Costco (COST)

The stock has made quite the comeback as money desperately rotated into staples. Much of the rotation has to do with the “collapse of white collar” and “the end of software” fear-frenzy, but so long as that persists and the chart looks like this, it is hard to argue against a bullish bias.

If you are a trader, I don’t like that the trend in momentum — MACD and RSI — aren’t confirming the trend in price. Assuming MACD and/or RSI do not change to reflect the trend in price, I would fade a breakout above the 6-month high around $1028.

For those interested in investing, remember the name of the game for COST is sales, membership growth, and membership retention. I attribute much of the weakness in the stock from June to December to concern over membership retention. If this rate perks back up, valuation won’t matter again. Maybe a return to form on that metric is what the market is sniffing out.