Key

Macro Economic Events

Corporate Earnings

High Importance

See Note Section Below For Additional Insight

Monday

Dominion Energy (D) | BTO

Tuesday

Home Depot (HD) | BTO

Wednesday

Nvidia (NVDA) | ATC

TJX (TJX) | BTO

SaaS Reports | ATC

Thursday

Initial Jobless Claims | 216k est. & 206k prior | 0830

Coreweave (CRWV) | ATC

Zscaler (ZS) | ATC

Friday

Producer Price Index (PPI, January) | 0830

- Core YoY: no est. available & 3.3% prior

- Headline MoM: 0.3% est. & 0.5% prior

- Headline YoY: no est. available & 3.0% prior

- Core MoM: 0.3% est. & 0.7% prior

Gorilla Thoughts

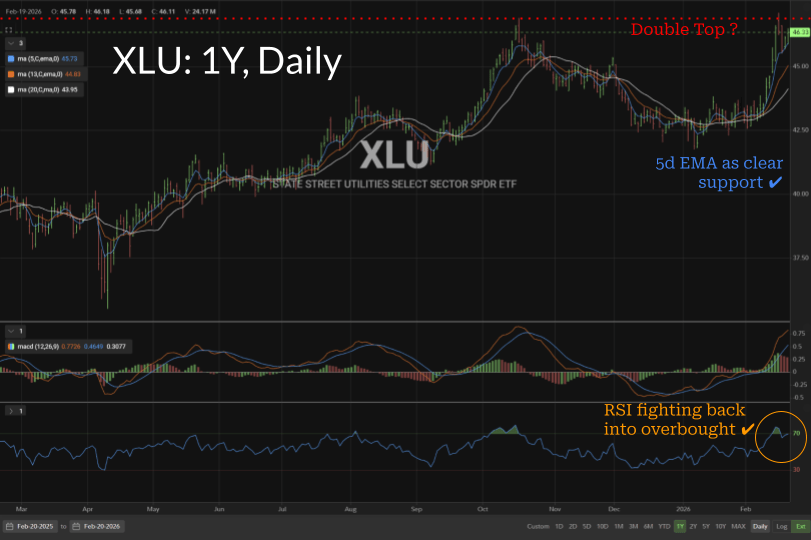

Dominion Energy (D)

Whether it be AI-energy demands, the moat of hard assets against AI disruption, falling yields making their dividends more attractive, or some sort of safe-haven bid… utilities may finally be getting the rerating I thought they might… after giving up on my pick in the sector a month too early.

Thankfully, it may not be too late to simply play the sector with the XLU. The only fear exists in the potential for a double top. That said, Dominion – which reports and was my pick in the sector – looks a little better: no double top, already a breakout in progress. Perhaps, the earnings will provide an opportunity for me to get back into Dominion.

Home Depot (HD)

SCOTUS struck down the IEEPA tariffs as unconstitutional last week. Why does that matter for HD? In theory, the inflation side of the Fed’s dual mandate got a little easier. While the estimates on how much tariffs have increased inflation in the data (CPI, PPI, PCE, etc…) vary, no unbiased observer has an estimate of 0%. Less inflation risk makes it easier to cut, which benefits homebuilders and the like.

Worth noting that rate futures reacted hawkishly to the decision. I am not sure that will stick for long. My best guess is that the move is a hedge against the White House going economically nuclear (for lack of a better term) with Section 338 (which would open the door for tariffs up to 50%)? The language in that Depression-Era statue is fair strictly. So, if that is the case, I expect this sort of tail-risk ultimately gets priced out.

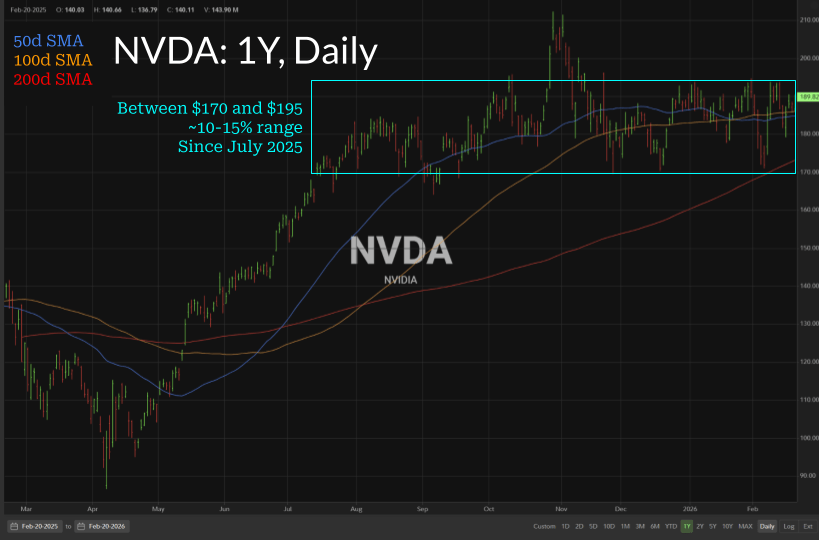

Nvidia (NVDA)

The upcoming report is the week’s most anticipated, and it will assuredly be impressive. A significant portion of the capex that has handicapped some of the “Mag 7” is going directly into Nvidia’s top line. Given this is known, we don’t need to waste time speculating on the quality of the report.

However, I cannot convince myself another amazing earnings will drive Nvidia beyond its seven-month consolidation range. Blockbuster earnings reports have been characteristic throughout this period.

Conversely, it would create an incongruent dynamic to penalize the hyperscalers for writing massive capex checks and penalize Nvidia for cashing them. Yet, the current negative sentiment surrounding all tech is strong enough that no post-earning price reaction should come as a surprise.

In a sentence, I do not anticipate Nvidia’s quarter as a catalyst to break its tight trading range; a new catalyst will be required for that to happen to the upside or the downside.

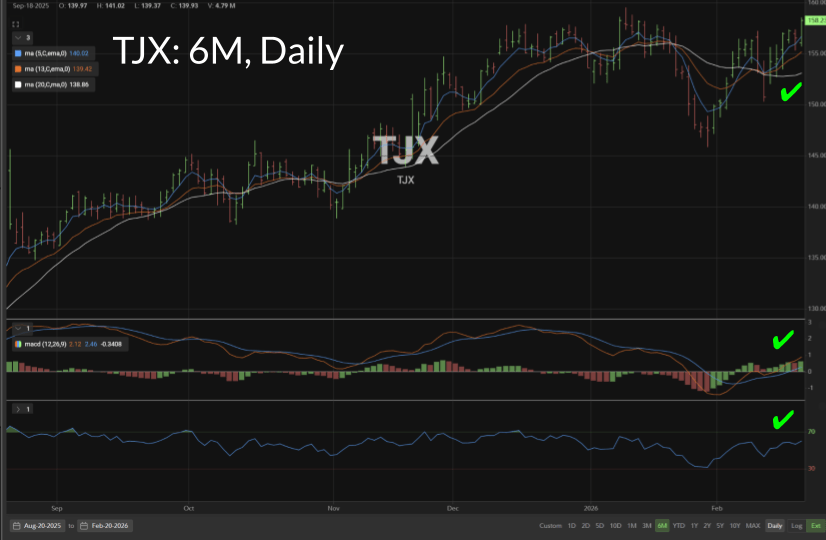

TJX (TJX)

I love TJX… specifically Marshall’s. I am always a visit away from their credit card… Excuse me. The stock.

Got to love what you see: above the short-term moving averages, green lights on MACD and RSI… it wants a new all-time high. That said, I would wait for the quarter. This name acts funny around the print. Management constantly under-sells so they can over-deliver. Not sure how the market is going to respond to that.

Saas Reports: Snowflake (SNOW) & Salesforce (CRM)

Software as a Service has been left for dead. Sadly, there is nothing either company can say or show at the earnings that will matter. Fear of AI disruption is the reason for the decline; earnings will not dispel those fears. Could we get a bounce on a good report? Of course… but, I’d be willing to bet any positive price action gets faded before the session closes.

That said, if you want to be an investor, you are certainly somewhere in the “buy low” phase of the “buy low, sell high” cycle. I have enough exposure via Microsoft, which – alongside NOW – I expect to be the first of the cohort to make a true bottom.

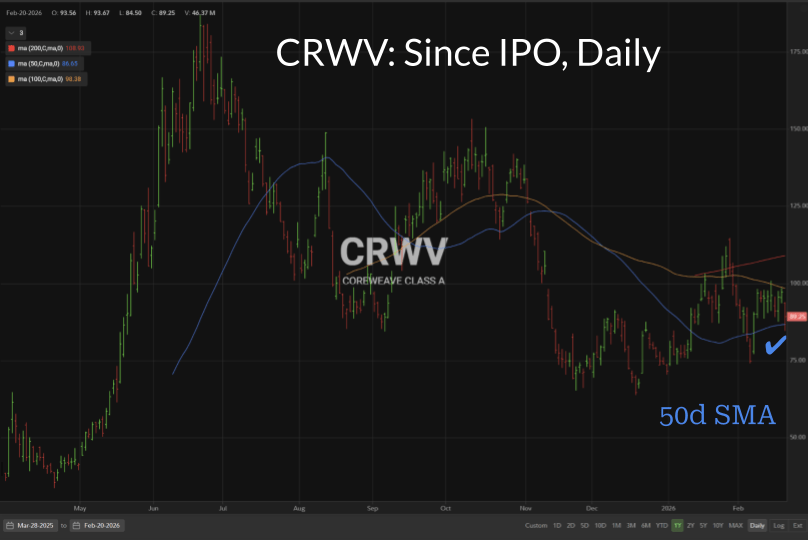

Coreweave (CRWV)

Courtesy of Blue Owl, Coreweave did not enter the weekend on a high note. Reports are that Blue Owl shopped debt for a CoreWeave data center… and lenders didn’t come. If you can’t get investors to take on the debt, it doesn’t portend well for the equity. I’ll waive my consulting fee to help out the team at Blue Owl: next time, market it as an AI Factory. It’s more provocative. Assuredly, lenders would have come for that.

Kidding aside, while the chart doesn’t look good, Friday’s action didn’t break it. Yes, it lost the shorter-term MAs I watched, but caught a bid at the 50d SMA. That counts for something. However, similar to my comments on SaaS, earnings didn’t cause the slide; it is unlikely earnings alone can sustainably fix it.

I’m not in the name nor am I interested. I know many made a lot of money trading this stock in 2025. CRWV as an example of the point I want to make: the kind of stocks that made you money in 2025 have yet to do the same in 2026. Consider fishing in different ponds until the weather changes.

Zscaler (ZS)

Anthropic launched Claude Code Security, a cybersecurity product that scans code for vulnerabilities and suggests fixes. Static vulnerability scans have existed for a while. The nuance here is reliable, suggested fixes. Fixing the vulnerabilities takes time and is what companies pay cybersecurity experts the big bucks to do.

AI can do a lot of great things. I use it frequently. Consequently, I have firsthand knowledge of its clear limitations. Too often it is devastatingly wrong. It has not earned blind trust for even small tasks… let alone for tasks of greater importance. In the short term, I can see AI disintermediating all things mediocre. However, I am not convinced it is capable of replicating expertise in it’s current state.

So, for those convinced AI will disrupt cybersecurity, which means companies will end their relationship with expert incumbents to pursue an in-house strategy, don’t fool yourselves into viewing this as a trade-off without cost. It will require time, money, and introduce a new dimension of reputation risk:

- You’ll need to staff and train at least a handful of salaried cybersecurity experts, which run—not including benefits—around $150k per head a year.

- In addition to training and hiring personnel, you’ll need to create an in-house architecture for cybersecurity from scratch and work to integrate that architecture with your legacy systems.

- Once that is finished, if something goes wrong, it is your reputation on the line. You are now the fall guy.

I am on the record: I find the AI-cybersecurity bear thesis as ridiculous. As you can probably already tell, those feelings haven’t changed. In fact, I believe the opposite will be proven out over time.

AI means more complex cyber threats. More complex threats means more demand for true cybersecurity expertise.

In my opinion, the target customers of this new product should be the CrowdStrikes, Zscalers, Palo Altos, and Fortinets of the world. If you can increase the efficiency of their experts, then these companies don’t need to be as aggressive on their headcount:

- CRWD → 10,000

- PANW → 16,000

- FTNT → 14,000

- ZS → 9,500

That said, this market is shooting first and asking questions later for everything even tangentially at risk of any AI disruption. If you want to start accumulating shares of cybersecurity stocks, make a plan to average your way into these names. Use time. Use price. Whatever plan you can stick to. I wouldn’t recommend going all in all at once because I don’t think we’ve made it to “later” yet.