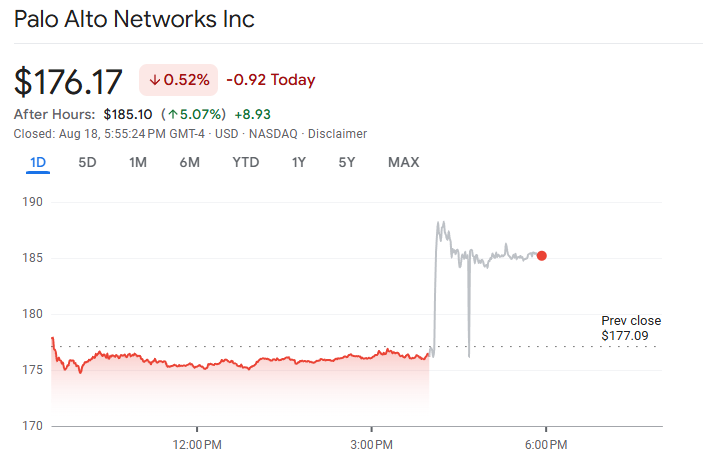

Palo Alto (PANW) just crushed it:

TLDR:

- Revenue: Beat

- Earnings: Beat

- Guidance for Upcoming Quarter: Beat

- Full Year Guide: Beat

Doesn’t get much better than that.

And… as of 6 PM, the market likes it, up 5%. Although it isn’t lost on me that expectations were lower for PANW given the 14% drawdown, this earnings season, if you see green once the number is out, you’ve done something right. Fingers crossed, this sticks… especially because I have been putting money to work at this level (100W SMA).

AI-Driven Software Skepticism

Over the past couple of weeks, the market has batted a skeptical eye at software stocks. The thesis: AI-driven headcount reductions are a structural headwind for pay-by-seat and pay-by-license software business models (per-seat).

Smaller Workforces / Fewer Jobs / Fewer Hiring → Fewer Seats → Less Revenue

Revenue growth will lag unless vendors offset with price increases, bundles, or a shift toward usage-based pricing. And without immediate clarity on pay-by-seat software companies, this market has decided to “sell now and ask questions later.”

Per-Usage versus Per-Seat

While I agree that the per-seat model is operating at a disadvantage, I disagree with the initial response of selling all software. Not all software companies use that business model. Pay-by-usage or pay-as-you-go (per-usage) is another way to go. Palo Alto’s business model includes per-usage components, which showed in its strong results. In my opinion, this report should be enough to remind the market of the diversity within the sector, both by business model and sub-industry.

The market isn’t stupid. Sometimes, it just needs a reminder of what has been so obvious to those at GwG.

Even if “pay-by-seat” models don’t prove to be losers, it is easy to understand how “pay-by-usage” will be relative winners. Although AI may decrease headcount, it will increase workload. When pricing keys off consumption (requests, tokens, jobs, vCPU-seconds, GB-hours, endpoint-hours), revenue scales with activity. Fewer humans can still generate more API calls, batch jobs, embeddings, vector searches, and background automations. CFOs can cut idle seats, but they cannot cut necessary usage without breaking outcomes.

Don’t believe me? How else do you explain Microsoft Azure, a pay-by-usage service, growing 39% off a multibillion-dollar base?

Below, you’ll find a list of some clear winners and losers based on our business model distinction. You’ll notice that, on a relative basis, the market hasn’t been punishing one group as much as the other. That said, I believe the implications of Palo Alto’s quarter has the potential to change the state of the software trade:

Current: Sell all software, but be less aggressive cutting the good pay-by-usage names.

New: Keep trimming pure pay-by-seat exposure, and start rebuilding positions in pay-by-usage where value and unit economics are still obvious.

Winner and Losers

Pay-by-Seat → Losers

- Salesforce (CRM)

- Monday.com (MNDY)

- Okta (OKTA)

Pay-by-Usage → Winners

- Certain Cybersecurity: Palo Alto (PANW), Crowdstrike (CRWD)

- AWS from Amazon (AMZN)

- Azure from Microsoft (MSFT)

- DropBox (DBX)

If you’re still here and liked what you read, could you do me a favor? Consider subscribing to my website by signing up below for insights delivered directly to your inbox. If that doesn’t suit your fancy, consider dropping me a follow on LinkedIn, or sharing my work. Thank you for reading.