What is Silicon Valley Bank (SVB)?

SVB, the bank of choice for many of the U.S.’s most promising and innovative startups, was the 16th largest bank in the country.

What Happened?

Due to liquidity and insolvency concerns, SVB was shut down by California regulators. The FDIC has been appointed receiver, granting them the power to transfer any asset of the failed institution without approval or consent. The FDIC will retain this power until the situation is resolved. Resolution will either come with SVB being absorbed (bought) by another, healthier bank, or with the FDIC selling/collecting the assets of the failed bank and settling its debts, including claims for deposits in excess of the $250,000 insured limit.

How Did This Happen?

SVB’s client base is largely Silicon Valley startups and IPO-bound companies. The last two years have not been friendly to either of those groups. During this difficult period, SVB’s clients have been steadily withdrawing their deposits to keep their businesses afloat as economic conditions worsened. Over time, this left SVB short on capital (cash). Eventually, capital levels fell low enough to force SVB to sell all of its “available-for-sale bonds”.

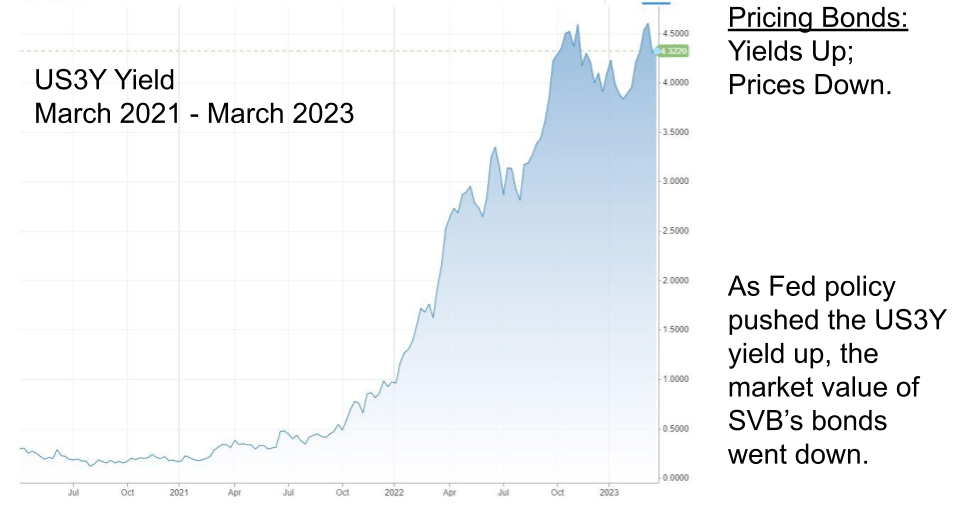

CNBC on-air programming reported this particular bond portfolio had a large exposure to three-year U.S. treasuries (US3Y). Since early 2022, the Fed has been raising the Fed Funds rate, which caused the US3Y yield to rise with it. The relation between bond yields and bond prices is inverse: as yields increase, prices decrease. Consequently, when SVB sold that bond portfolio, they realized a $1.8B loss.

To make up for the shortfall, management announced they were looking to raise another $2.25B to “shore up its balance sheet”. This announcement scared SVB‘s clients, causing a bank run – large groups of depositors simultaneously withdraw their money based on fear that the institution will fail – exacerbating their capital position. As news of the bank run spread, SVB’s capital raise failed as no one wanted to buy stock in a bank that appeared to be on the brink of collapse. The bank run intensified once the result of the capital raise became public. Soon after, California regulators decided to shut down the bank before the situation could escalate further.

Why Does It Matter?

For the first time since the Great Financial Crisis (GFC) in 2008, a bank failed, and the Fed broke it.

By no means am I absolving SVB of their role in their own demise. The Fed has been saying “higher for longer” for a while. There is no reason SVB’s management should not have had a risk management policy in place for this foreseeable scenario. However, the fact remains that the Fed created the financial conditions that stressed SVB’s client base and aggressively raised rates enough for an investment in treasuries, risk-free assets, to result in $1.8B loss. As a result, it can be argued that SVB would not have failed if not for the Fed’s restrictive monetary policy implemented to fight inflation.

Response Function

f(Investors)

In the immediate aftermath, investors need to determine whether SVB represents contagion risk: the risk that financial difficulties of this bank spill over to a larger number of other banks or the financial system as a whole. To put it differently, investors need to determine if what happened at SVB can happen at other banks or will cause other banks to fail. On a related note, investors need to consider what this means for SVB’s clients and all the businesses those clients work with.

GwG Insight

In my opinion, SVB will prove an idiosyncratic (singular, outlier) event for the banking system. SVB has a unique client base that was disproportionately harmed by Fed policy. Furthermore, the big money center banks – J.P. Morgan, Wells Fargo, etc… – are subject to stricter regulation, which means they are better capitalized, tested more frequently, and practice stricter risk-management policies.

Given its size as the 16th largest bank in the U.S., it is hard to imagine an outcome where everyone else comes out unscathed. The ripple effect is most likely to stem from businesses whose money is frozen at SVB. To continue operating, these companies will need to raise money by taking out new loans at incrementally higher rates, or by selling additional common stock, which dilutes shares. The former increases default (bankruptcy) risk, the latter tends to decrease share prices. I think this risk is limited to companies that were overly dependent on SVB and the businesses that have deep relationships with those overly dependent companies. Since the majority of these companies are in technology, I do not expect much spill over into other economic sectors. This contributes to my thesis that SVB will be relatively contained and does not pose a systemic risk to markets.

f(The Fed)

This means the Fed hikes 25 bps or pauses at the March 22nd FOMC Meeting. CPI will update the inflation picture on Tuesday, but no one needs to see it to know inflation is still too high. SVB’s demise has shaken confidence in the banking system. Repairing that confidence deserves priority over inflation. It is impossible to understate how momentous this event is: The first bank failure since the GFC. Furthermore, there are incremental factors that justify a less hawkish move:

- Payrolls showed no spike in wage inflation.

- Silicon Valley Bank’s failure likely means a slowdown in the creation of high-paying jobs in the tech sector, which should contribute to lower inflation data in the intermediate term.

- February CPI, even before release tomorrow (3/14/23), is too “old” in the aftermath of SVB.

GwG Insight

The Fed’s goal is to cure inflation without killing the economy. If you sacrifice the banking system to cure inflation, you kill the economy. A banking crisis would be more detrimental than an inflation crisis. It is not a viable trade-off. If anything, the Fed should start evaluating alternative methods of slowing the economy. The Fed could increase the reverse limit requirements, which would reduce the amount of capital big banks have to make loans.

Although I believe SVB will be an isolated incident with limited contagion, it would be inappropriate for the Fed to take that risk. Therefore, a 25 bps increase or pause at the March FOMC appears most appropriate. Right now, I am leaning toward 25 bps because it allows the Fed to put additional pressure on inflation and soothe banking system sentiment by showing restraint with the interest-rate tool that contributed to SVB’s failure.

Leave a Reply